We know that when a new client joins us, they often have a lot of questions they want answering. To help you out, we've put together some of the most commonly asked questions we get.

Of course, if you have any questions that aren't covered by the answers below, or you would simply like to talk about how these answers relate to your specific circumstances, you are always welcome to pick up the phone or email your questions and we will give you a straight forward, quick clear answer.

What qualifications do you have?

We are Chartered Accountants and proud to be members of the Institute of Chartered Accountants of England and Wales (ICAEW).

Are you regulated?

The accountancy firm is not actually a regulated industry - anyone can set themselves up as one, however only accountants who are members of the ICAEW can call themselves "Chartered Accountants".

All accountants need to comply with HMRC's anti-money-laundering regulations but ICAEW member firms are bound by a much higher standard of professional, ethical and technical behaviour.

A Practicing Certificate is the ICAEW's licence to allow their members to offer their accountancy services to the public. Only members with a Practicing Certificate can offer their services to the public and it takes many years of exams and then even more years experience before they will allow their members to hold a Practicing Certificate.

I have an existing accountant - is it hard to switch?

It's really easy to switch accountants, especially if you are using cloud accounting software - you just need to invite us in (we'll show you how!).

If your existing accountant is a qualified accountant they will have a code of practice specifying how transfers should happen. Sometimes your existing accountant may be slow, but a reminder from another qualified accountant of their professional obligations regarding what is known as "professional clearance" is usually enough to get even the most unresponsive accountants to send over the relevant information.

Will I be charged for phone calls, emails and other queries?

For quick queries, or items covered by the services we are providing, generally no.

Where your queries are really a larger piece of work then we would provide a separate engagement for that work and agree our fee accordingly.

We will obviously discuss this with you before any fees become chargable.

Will I be locked into an annual contract?

No - our contract has a 30 day notice period meaning that if you want to leave you can do so. The 30 day notice period is only really to allow us to finish any work and provide sufficient time for your new accountant to get up to speed.

When will my year end accounts be ready?

We start your year end accounts as soon as we are able to. Where we have access to your accounts via a cloud accounting software we should be able to start work on them as soon as you have updated the bank.

The deadline for filing your accounts is normally 9 months after the year end, but we like to have your accounts completed as soon as possible to give you the most relevant and timely information for you to make decisions on.

When will you start my personal tax return?

The tax year end is the 5th April each year. We start work on your personal tax return as soon as we are able to and will contact you in April to get the process started.

Your tax return is usually due by the 31st January after the tax year end, but we tend to get most returns filed well before then so that you have clear visibility as to what your tax liability is early on, so that you can make sure you have enough put aside to pay it

Where can I get my Unique Tax Reference (UTR)

Your UTR is required in order to file your tax return. Almost any letter from HMRC to you will include your UTR, although it may be buried within a longer reference code in that letter. If you send it to us we should be able to extract that code.

For your company you can request they resend this to you (https://www.tax.service.gov.uk/ask-for-copy-of-your-corporation-tax-utr). They will send it to your registered office.

If you don't have access to your registered office, but do have your Companies House authentication code, you can change your registered address online (https://www.gov.uk/file-changes-to-a-company-with-companies-house).

If you don't have access to your registered office and also don't have your Companies House authentication code (assuming your old accountant is not responding) there is a way to change the address without it. Once the address is changed you can then ask Companies House to resend your authentication code. I've written a post on it here: How to change your registered address when you're locked out

What is my Companies House Authentication Code and how can I get it?

Your Authentication Code is a unique code for your company (basically a password) that allows you to make changes to your company at Companies House, and is required to file your accounts.

It's a 6 digit alphanumeric code and would be sent to your registered address when you first set up the company.

If you don't have it Companies House will resend it to your registered address (https://www.gov.uk/guidance/company-authentication-codes-for-online-filing)

If you don't have access to your registered office and also don't have your Companies House authentication code (assuming your old accountant is not responding) there is a way to change the address without it. Once the address is changed you can then ask Companies House to resend your authentication code. I've written a post on it here: How to change your registered address when you're locked out

My registered address is at my existing accountant so I can't receive any mail to do with my business - what should I do?

You will need to change your registered office to another office you have access to.

If you don't have access to your registered office, but do have your Companies House authentication code, you can change your registered address online (https://www.gov.uk/file-changes-to-a-company-with-companies-house).

If you don't have access to your registered office and also don't have your Companies House authentication code (assuming your old accountant is not responding) there is a way to change the address without it. Once the address is changed you can then ask Companies House to resend your authentication code. I've written a post on it here: How to change your registered address when you're locked out

Do I need to send you in all my receipts

No. Please don't! Unlike the somewhat more traditional accountants we don't adopt a parent-child relationship and tell you what you may or may not do. Rather we advise you on what the rules are and how they apply to your situation.

Most accounting software has somewhere for receipts to be stored, and in most cases it is good to attach the receipts to the relevant transaction in the accounts.

It's important that you do hold on to your receipts as evidence of what you spent money on. If you choose a different system for keeping hold of your receipts make sure you are consistent and that there is an order to allow you to find them, should you ever be required to.

Sometimes we will request copies of certain invoices or receipts to allow us to better understand the nature of the transaction.

Do I need to check with you before I pay a dividend

No, we don't give you permission, however we can help you work out whether you can pay a dividend and if so how much.

Dividends must be made out of "distributable profits", which means before making a dividend you should bring your accounts up-to-date, including taking account of any corporation tax you will be due to pay, but have not yet actually paid.

FreeAgent is by far the best software that handles this as it puts in an estimate of your corporation tax throughout the year, and has a section that tells you how much you can pay at any given point.

Other systems, such as Xero or QuickBooks don't do this, and so care must be taken whe using these systems.

You can find out more about this here: A small business owners guide to dividends

How should I get my money out of the company?

There are a variety of ways to get money out of your business which we can advise on.

The three main ways are

Each has their own tax consequences so its important that you take advice as to which methods and at what level is the most appropriate for you.

There are, of course, other methods of getting funds out of the business such as benefits in kind, loan interest and pensions. Again, having an accountant that understands your personal and business circumstances is vital to ensure that you are able to maximise the amount of money you take home.

Can my partner be a shareholder?

Absolutely they can. It is important to ask the question why you would want them to be but it is certainly possible. There can be many benefits in bringing on a spouse into your company but it is absolutely vital that it is done in the correct way, to avoid future potentially large and unexpected tax bills.

We can advise on the most appropriate structure for you and mechanism for getting from where you currently are to that final structure. This may be a minority shareholding, an alphabet share structure and/or bringing them on as an office of the company (i.e. a director).

How do I go about paying myself a salary?

In order to pay yourself a salary you will need to be registered for PAYE and make monthly, (or weekly if you are paying yourself weekly) returns to HMRC. You will need professional software to make these submissions, or use HMRC Basic PAYE tools to do so.

Getting set up with a PAYE scheme is a relatively simple matter. Usually, if you do not have a PAYE scheme set up the money you pay yourself would likely be classified as dividends or a director's loan, which can have some nasty tax consequences.

With The Accounting Studio, we will run your payroll each month, create your payslips, let you know how much you should pay yourself, and anyone else on your team, let you know how much to pay HMRC and any pension scheme you have set up, and file the return with HMRC. It all runs very smoothly..!

I've spent some money on the company before I set it up - what can be done about this?

When you have spent money on the company, even before it was set up, this, in most cases can be treated as "pre-trading-expenditure" which means it is treated as if the expenditure had been made on the day you started trading.

We are more than happy to advise further on the eligibility of this sort of spending for you.

Should I be registered for VAT?

The basic rules are that if your taxable turnover is over the VAT threshold (currently £85k) within the last 12 months (on a rolling 12 month basis) then you would need to be registered for VAT.

You can also register on a voluntary basis and there are a variety of factors to take into account when making this decision, such as who your customers are, whether they are based, what goods or services you provide etc

It can be quite complicated working out what you "taxable turnover" is - what to include and what to exclude

We are are happy to assist you in establishing whether you need to be VAT registered on a case by case basis

How do I pay a dividend?

We've written a blog post on this question to give a more full answer and we recommend you read that: A small business owners guide to dividends

The short version is that you need to do the following:

- Bring your bookkeeping up to date (bank, invoicing, purchases, VAT etc) to calculate your profit before tax

- Estimate how much corporation tax you will need to pay on the profits you have made and deduct from your profit before tax to calculate your profit after tax

- Add to your profit after tax any profit or loss from previous periods

- Deduct any dividends already paid, to leave what is know as "distributable profits"

- Consider whether you have enough profits to make a dividend

- Declare the dividend

- Pay the dividend (just a bank transfer)

- Issue a dividend voucher

If this sounds like a lot, most accounting software will do most if not all of these steps for you.

Can I make my company dormant?

Dormant accounts can be filed if certain conditions are met. Working out whether these conditions have been met is a backwards looking process. So you don't declare you company to now be dormant, you assess whether your company has been dormant.

We wrote a post on this for more detail: Essential Guide to Dormant Accounts

Do I need to retain paper copies of my receipts?

You do need to retain copies of your receipts, but they don't need to be paper copies. We recommend that most clients attach electronic versions of their receipts on their cloud accounting software to the actual transaction to which it relates.

You can also keep paper copies, either as well or instead, but make sure you have a good system for finding them (eg, sorted into monthly batches) so that they are easy to find should you ever need to

Do I need to set up a personal/business tax account?

Yes.

A business or personal tax account is an online account on gov.uk where you can see some really important things related to your tax.

The business tax account would be for your company and is where you can control your corporation tax, PAYE and VAT. You can sign up or sign in here (https://www.gov.uk/guidance/sign-in-to-your-hmrc-business-tax-account).

A personal tax account is for you personally and where all your personal tax information is brought together in one place. You can use it for updating HMRC of changes (eg address), payment of your taxes, and checking on your national insurance contributions towards you state pension. You can set it up here (https://www.gov.uk/personal-tax-account).

Do I need to set up a employee pension scheme?

Where the only employee is you and you are the director, there is no requirement for you to be "auto-enrolled". As soon as you have staff you will have an obligation to consider your pension requirements.

It's worth taking a look at NEST for more information on this, which is a pension scheme set up by the government to allow all employers access to a pension scheme that is compliant for auto-enrolment.

I've loaned some money to the business. How can I get it back?

When you put money into the company, the initial amount is used to pay the share capital that has been issued. Additional funds will then be treated as money loaned by you to the business. These funds sit in the accounts until such as point as the company can repay them.

Whilst many do not do this, and whist the director, and the shareholder may be the same person, it is worth considering setting up a loan agreement to agree how the loan should work. This could be drafted by a solicitor, or you could use one of the online legal document providers such as LawDepot, or RocketLawyer.

From a tax perspective, as the repayment of the loan is simply the settling of a debt, there is no tax consequences to extracting funds in this way (unlike other method such as dividends or salary).

How do I claim expenses?

Expenses are where you personally have incurred costs on behalf of the company and where the company needs to reimburse you for that expense. There are some slightly more complicated items, particularly around travel and food, but in general expenses can be reimbursed without there being any tax consequences. You will need to ensure that you submit sufficient evidence for expenditure (i.e. receipts).

Exactly how the expenses get processed will depend on the system

- FreeAgent has a great expenses module where you can make the claims split between normal expenses, and mileage. It calculates the mileage claim making sure that the correct rates are used. These sit on the accounts until repaid. If you opt to use the Smart User Payment feature it will even allocate payments to you in the order of salary, then expenses, then dividends, which is quite a neat little feature not found in other software

- Xero users could use the expenses module, which may be a bit overkill if its just you making a claim. I would recommend raising a bill itemising the expenses, and then making a bank payment for the amount, which Xero will then likely match up in the bank rec. This method will work for most other cloud accounting systems.

You need to make sure that there is sufficient detail in the claim and that the claim matches the expense amounts, otherwise there can be some problematic tax consequences.

Do I need a bank account for the company?

Yes.

It's really important to ensure that your business and personal money stays separate to avoid chaos and either accidentally claiming personal costs, or missing out on claiming costs that you should have.

If company income goes to your personal bank account, unless it is accounted for correctly, it can create some significant and expensive tax issues.

It's much cleaner to make sure that business expenditure goes through the company bank account, and personal expenditure goes through your personal account, to avoid getting mixed up.

Is it better to spend money through the company, or expense it?

Technically, it doesn't really make much of a difference (with the strange exception of some expenses when making an R&D Tax Credit Claim), but administratively and organisationally it makes much more sense to try to ensure that all business expenditure goes through business bank account, and all personal expenditure goes through a personal account (i.e. not the business account). Otherwise it can take a lot of unpicking of transactions, or a long time spent making expenses claims in order to get the money back.

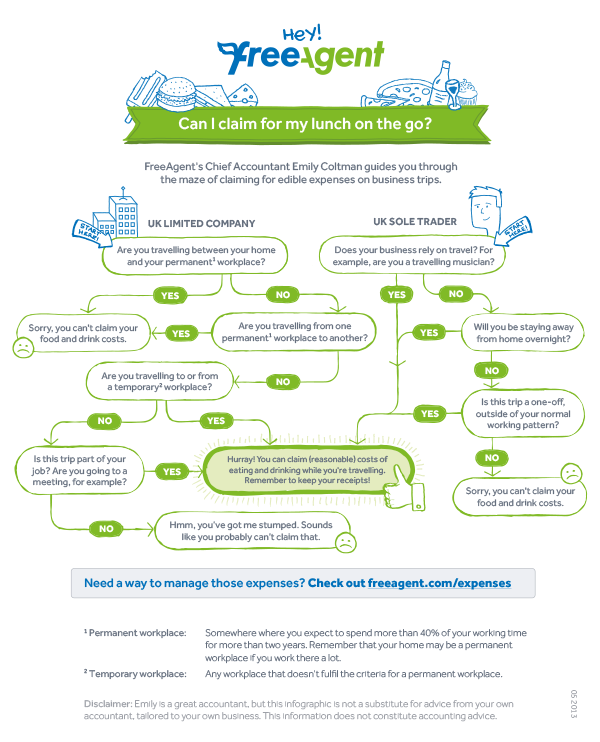

When can I claim my lunch?

The general rule is that if the trip counts as a business trip then you are eligible to claim food.

FreeAgent have produced a brilliant infographic here:

View the full image at FreeAgent

Can I employ my partner/spouse and save some tax?

Yes. But your partner needs to be doing real work for the business and the salary or payment needs to be what you would pay someone if they were not your partner or spouse. If HMRC look into your affairs and consider it to be artificial, they might consider it to be a "settlement" and effectively push that salary payment back on to you. You would then be hit with possible fines, interest and surcharges for having not declared that income at the right time and paid tax on it.

Can I claim for my broadband through the company

Sadly no (in most cases). Or at least without it costing more in tax than it would save.

To establish for certain if you could claim for you broadband through your company you need to work out what the marginal additional cost being incurred is. In other words, what additional expenditure are you incurring as a result of your work in the business? For most people they would have their home broadband even if they were not using it for business, and if that is the case, then you can't claim for it without incurring more tax costs than you would be saving.

Can I claim for my mobile phone through my company

The answer is yes, but only if it's done right.

The contract needs to be in the company name, not the individual's name.

If the company pays for an individual's contract it will be considered undeclared salary so its important to get this point correct.

Also, in order for the expenditure not to be treated as a benefit in kind, you would only be able to provide one company mobile phone per person.