As a small business owner, you have a lot of important decisions to make. One of the biggest decisions you’ll face is how to structure your business. There are several options to choose from, but one that you should definitely consider is setting up a limited company.

Now, before we dive into the benefits of limited companies, let’s define what we mean by “limited company.” A limited company is a type of business structure in which the owner’s liability is limited to the amount of money they have invested in the company. This means that if the company gets into financial trouble, the owner’s personal assets (such as their home or savings) are protected.

In the UK these are normally set up and registered at Companies House.

So, why would you want to set up a limited company for your small business? Here are a few reasons:

Limited liability protection: As we mentioned earlier, one of the biggest advantages of a limited company is the limited liability protection it offers. This can be especially important for small business owners who don’t have a lot of personal assets to protect. If something goes wrong and your business is sued or gets into financial trouble, your personal assets will be safe.

Tax advantages: Another reason to consider setting up a limited company is the potential tax advantages. If you’re self-employed and running your business as a sole trader, you’ll be taxed at the personal income tax rate on your profits. However, if you set up a limited company, your business will be taxed at the corporation tax rate, which is currently 19%. This can potentially result in lower taxes for you as the owner.

Professional image: Let’s face it, running a small business is tough. You’re constantly hustling and doing whatever it takes to get ahead. But as you grow and start to bring on more customers and partners, it’s important to project a professional image. Setting up a limited company can help with this. It shows that you’re serious about your business and that you’re willing to take the necessary steps to protect it (and yourself).

Potential for growth: As your small business grows and starts to bring in more revenue, you may decide that you want to take things to the next level. Maybe you want to hire more employees, expand your product line, or open a second location. Whatever your goals, a limited company structure can make it easier to attract investors and raise capital. This can be especially important if you don’t have a lot of personal savings or assets to use as collateral.

Now, I know what you’re thinking: “But setting up a limited company sounds like a lot of work!” And you’re right, it does require some extra legwork. But trust me, the benefits are worth it. You’ll have peace of mind knowing that your personal assets are protected, you’ll potentially save on taxes, and you’ll give your business a professional image.

If you’re considering setting up a limited company for your small business, my advice is to seek guidance from a financial advisor or accountant (er – like us). We can help you understand the process and make sure everything is done properly. And remember, the benefits of limited companies are just one piece of the puzzle. There are plenty of other factors to consider when deciding on the best business structure for you.

So, if you’re ready to take your small business to the next level, consider setting up a limited company. It may require some extra effort upfront, but the benefits are worth it in the long run.

A dividend is a way of the company paying out its profits to its shareholders. They are paid out of “distributable profits” of the business, which broadly means the accumulated profits of the company that have not yet already been paid out to shareholders. This means that when you pay a dividend it is paid from profits where corporation tax has already been charged, even if the corporation tax has not yet been paid.

How are dividends taxed?

As mentioned above, dividends are paid out of “post tax profits” – i.e. after corporation tax is paid. Unfortunately that does not mean that personal tax is not also due. By the time dividends are ready to be paid they will already have suffered corporation tax of 19% (at the time or writing).

When dividends are paid to individuals they are taxed a second time, and here is how:

The first £12,570 (2022/23) of income that you earn from all sources is exempt from income tax. If you’ve had salary or interest as well, this will use up this band first. Whatever is left after salary and interest can be used against your dividends. This first £12570 is tax free

Dividends also have a special band call the dividend allowance which means that for the next £2000 you will not pay any income tax as well, however it does use up some of your basic rate band (see below).

After this, for the rest of the basic rate band you will pay only 8.75% on your dividends

In the higher rate band, you will pay 33.75% dividend tax and above that, it starts to get super complicated so it’s worth calling us to discuss.

How do I make a dividend?

In order for a dividend to be legally sound there are certain formalities that need to be undertaken. Broadly, they need to be declared, and authorised correctly, they need to be calculated correctly (so that in a normal situation a 75% shareholder would receive 75% of the total dividend, and a 25% shareholder would receive 25% of the total dividend), and they need to be paid and documented correctly.

HMRC is interested in whether the payment is genuinely a dividend or not. If the correct company law procedures have not been followed then any payments may be treated as salary, bonus or director’s loan – these may incur higher tax rates, NI costs and could also result in the issuance of a penalty for not submitting your payroll correctly, hence HMRC’s interest. Its important therefore to get the paperwork right and to ensure that there is no ambiguity over the status of any payment made to you

Legal

Interim vs final

There are basically two types of dividends – an interim dividend, which the directors declare, and a final dividend which the directors declare but which is then voted on by the shareholders. The key distinction is related to the deemed timing of the dividend. The date of an interim dividends is deemed to be when the dividend is paid, however, with final dividends it is when the dividend is approved. This matters for the timing of dividends around tax year ends.

Resolutions

Both types of dividends will require a board resolutions, however a final dividend also requires a shareholders resolutions as well.

Dividend Voucher

A dividend voucher is effectively a receipt that the company issues for the dividend. It’s the final formality required in terms of paperwork to make a dividend legitimate

Practical

Distributable profits

You can only make dividends out of distributable profits. If you try to make a dividend where you do not have enough profits to do so it would be considered an “illegal” dividend and be treated either as a loan to the shareholder/director, or as wages. Both have nasty tax consequences so it is important to check you have enough funds to do this. Don’t forget to take account of what corporation tax you may need to pay when considering this.

Dividends to multiple shareholders

Unless you have set up an alphabet share structure, or something similar, the default position is that dividends should be paid out according to each shareholders ownership percentage. Where there is one shareholder, this is unproblematic. However where there are multiple shareholders, there can sometimes be the temptation, for tax purposes to pay different levels of dividends. This can cause some major issues from a tax perspective, particularly if the other shareholder is a family member.

It is possible to do this but it is an area where HMRC have had a lot of success in challenging businesses and therefore before taking any such action its important that you take appropriate advice.

Common Errors that can lead to benefit in kind tax bills

I decided to write this article as I would find the same myths and misconceptions arising time and again with clients from all walks of life. Often is was due to bad or no advice have been received in the past, before they joined The Accounting Studio, and usually the ideas are quite sensible, but unfortunately wrong, or more likely incomplete.

The problem with hidden benefits in kind is that regardless whether you were aware of it or not, you are still expected to report them to HMRC on time and pay the tax, with some quite large fines for any breaches.

So without further delay here are my top error-creating-myths that I am going to try to address today…

My company can pay for my mobile phone, right?

Sort of. Your company can provide you with a mobile phone and you can use that phone personally, but the contract has to be in the company name, not the individual. Just transferring the direct debit or payment for it is not enough, even if it is only used for work. The contract must be in the company name.

The good thing about mobile phones is that although the company can provide you with one, HMRC have kindly allowed that the provision of a single mobile phone that gets used personally is not to be considered a benefit in kind – it is an “exempt benefit”.

I use my broadband for work, I can charge that to the company, right?

We see this question quite a lot, and it makes good sense. Interestingly, if you were self employed and not operating through a company, the broadband cost would be tax deductible, in some respect (and possibly all respects).

In a company, the situation is more tricky. The company can only reimburse you for the marginal additional cost that you have incurred (by which I mean any extra costs you have paid for as a result of your working for the business). With modern broadband packages, particularly home packages, there is no additional cost.

If you ask yourself whether you stopped working that the costs of the broadband would change, very likely it would be no. In this situation HMRC consider the cost to have “duality of purpose” , by which they mean that although you use if for business, but you also use it personally – there is no additional cost.

If you were to charge your broadband to the company HMRC would consider it to be undeclared salary, and taxed (and possibly fined for not declaring it) accordingly.

The short version is that it is almost never possible to charge your home broadband to the company.

If the company, however pays for the broadband, and the contract is with the company, then yes the company can do this. However, by allowing you to use the broadband (assuming you don’t still have a home broadband contract as well), this would be treated as a benefit in kind and also become taxable

I don’t have many expenses, so I can basically pay out whatever is in my bank to me as a dividend, right?

This is a surprisingly common view point and it takes a few steps before there is a benefit in kind but if you take this approach, but stay with me.

Companies have to prepare accounts using the accruals basis – basically meaning not only do you take account of what’s happened in the bank account, but you also care about things like what you owe and what you are owed. This means that the bank balance often serves as a very poor estimate of what you profit actually is.

Even in the simplest of companies, where there is just one invoice per month, and minimal outgoings, there is still corporation tax to be taken into account of. Some of the cash in the bank should really be put aside for paying the corporation tax and not be paid as dividends. If it is paid out it will be considered to be an “illegal dividend”, and this is where the problems start. I’ve covered it in more details here (A small business owners guide to dividends) but the illegal dividend would be reclassified as a director’s loan and often lead to an overdrawn directors loan account. Where this is over £10k at any point interest should be charged on it. If interest is not charged (which it almost always is not, as the director was no aware that the dividends were illegal), then the loan is treated as a beneficial loan on which a benefit in kind has arisen.

It sounds complex, and there are a lot of steps, but this is by far the most common scenario we see with hidden benefits in kind. We can normally sort this out, but it does happen more than you might think.

I can get my company to pay for X and it will be tax deductible, right?

No. Well, yes it will be tax deductible for corporation tax. But it will also be taxable on your personally. So you will save 19% corporation tax, only to pay 20% income tax (plus you will also owe 13.8% in class 1a National insurance tax. If you are higher rate tax payer the situation is worse. You will pay 40% on the costs, not 20%. It is not a good idea. Just say no, kids.

Any time I go anywhere on business I can claim the mileage?

Not quite anywhere but broadly yes, with some key conditions.

Home to work – its commuting – you can’t claim it.

Home to an office you often go to – if its a temporary workplace you can claim it. The test is whether you have spent, or are likely to spend, 40% or more of your working time at that particular workplace over a period that lasts, or is likely to last, more than 24 months. If the test is not met, it will be treated as a temporary workplace, and you can claim it

Home to not your office but somewhere that is basically the same place (like another business on the same street as you) – HMRC would call that commuting as it is substantially the same place – you can’t claim it

Home office to another office you regularly visit – can’t claim it (see the car crash that was the Dr Samadian case if you are in any doubt), unless it is a temporary work place

Wholly and exclusively – the trip must be wholly and exclusively for the purpose of business. If it is not then you can’t claim it

You can claim up to 45p per mile for a car for the first 10,000 miles, and then 25p per mile thereafter. There are also different rates for bicycles, motorbikes and additional passengers.

If you do happen to claim for mileage where you should not claim it, or you claim more than the amounts above, that would lead to a benefit in kind.

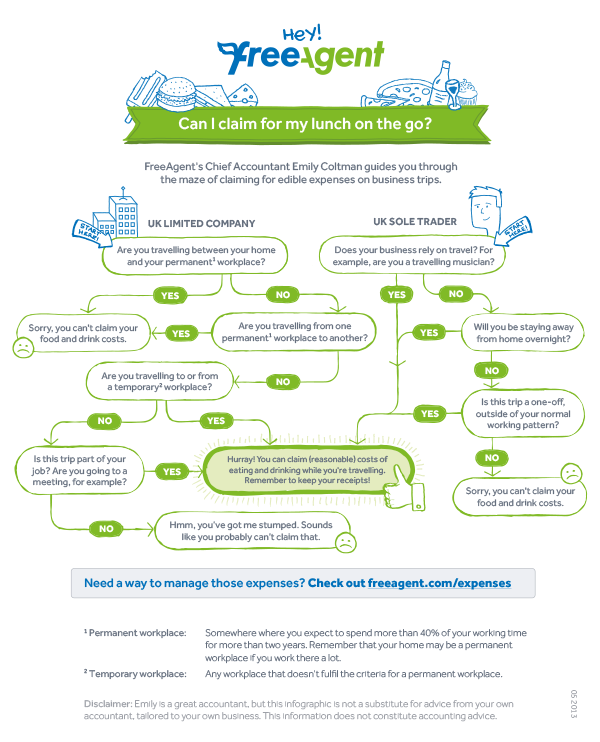

I can get lunch on the company whenever I’m out of the office, right?

The general rule is that if the trip counts as a business trip (see the above question) then you are eligible to claim food.

FreeAgent have produced a brilliant infographic here:

I’m having my meeting down the pub/in a restaurant/at a hotel so that it saves me tax

The company can pay for these things but it will be treated as employee entertaining. The company can claim the expense against it’s corporation tax charge. Where or not the expense is an employee benefit in kind depends on a few things.

To be exempt it needs to be

open to all your employees

annual, such as a Christmas party or summer barbecue

cost £150 (including VAT) or less per person

It might also be exempt if it falls into the trivial benefits rules

If it does not, then the spending will form a benefit on kind for the employee

(I should just point out that even if clients/suppliers etc are there it doesn’t help, and actually makes things worse, as these are not even claimable for corporation tax, unlike employee entertaining, which at least is)

If I visit a customer on holiday, I can claim the holiday as a travel expense, right

Sadly not. This doesn’t often get asked but it does crop up occasionally. The holiday, even if it had a business element would be caught by the duality of purpose rules relating to the wholly and exclusively rules. Basically, just tacking on a business meeting to a ski trip does not make it tax free. If the company paid for it, it would be treated as a benefit in kind and taxed accordingly

That’s not to say there is not something in this though.

For instance, going to a convention in Vegas (related to you business with a real business reason to go), but also relaxing by the pool whilst not at the convention, or spending the evening at a show or at a casino, would not breach the duality of purpose rules (although you would need to personally fund the show tickets/gambling etc). The point is that making the most of it whilst you are there is incidental to the real business reason – attending the convention. You had to stay over in a hotel, and do something with your time whilst not at work, and therefore you are able to get some benefit, that would not be treated as a benefit kind

Conclusion

So there you have it, some relatively common scenarios that may mean you end up with an unexpected tax bill due to benefits in kind.

When businesses are owned and run by the same person (the director is a shareholder) there are very often transactions between the company and the director. This could be the director initially putting money into the business to start it up, or injecting some cash when the company needs it. These sorts of transactions create something called a director’s loan account.

It may also be for wages that have been declared to HMRC but not yet taken, or expenses incurred by the director personally but not yet refunded to them.

The above are all transactions that increase the amount of money that the company owes the director.

However there are transactions that can send the balance in the other direction – simply drawing money out the business without declaring a dividend, or having the company the company pay for something personally for you. These are all obvious types of transaction which will either reduce the amount owing to the director, or will mean that the director actually owes the company some money.

There are other sorts of transactions that can sneak up on directors – illegal dividends are the most obvious transaction we see – where a director has paid more in dividends to themselves that company law allows them to – this would put the dividend in a repayable position.

The typical scenario is where the director has been only really paying attention to the bank account and paying themselves what is in the bank, forgetting that corporation tax is also due (this is incredibly common!)

Should the director owe the company money there are a variety of tax implications that apply.

A history of (tax) abuse

To understand the tax implications of the tax on an overdrawn director’s loan account its useful to know the context and history as to how it arose.

In the past some less that scrupulous directors would attempt to avoid paying income tax (or corporation tax) by lending themselves a large amount of money. As the money was a loan there was not income tax paid on it. This amount would continue to rack up until the directors decided to wind the company up, chalk the director’s loan as a bad debt, write it off and wind up the company.

The directors have the cash, and no impact was due. In our view this was never strictly legal but non-the-less did happen.

Section 455

To combat this HMRC brought in legislation that put the tax burden on the company – what is know as section 455. This means if there is a director’s loan balance outstanding at the year end the company has to pay tax at 32.5% on the increase in that loan. This was intended to ensure that HMRC got the tax even if the company subsequently was wound up.

There are a lot of rules around this, including the ability to get that amount back if the loan is repaid, or income tax paid on it.

Benefit in kind

On top of this s455 there is also something known as a benefit in kind that needs to be considered as well.

HMRC take the view that if you are borrowing money from the company, and not paying any interest on that money you are getting a benefit from the company and should therefore pay tax on the value of that benefit.

Thankfully this is quite a low level of benefit – the benefit is considered to be the tax you have not paid, which given the current official rate of 2.5% means that the overall tax you pay on this is often not all that much. On a £20k loan that interest should have been £500. Income tax at 40% would mean a tax charge of £200.

There is also a national insurance consideration that the company needs to pay on benefits in kind – Class 1a charged at 13.8% on the £500 totalling £69 (this £69 is tax deductible for corporation tax purposes so in reality works out to only cost £55.89). So on a loan of £20k a director might pay £255.89 per year.

The key issue with the benefit in kind that many directors find is not the cost, but remembering to do it, or paying an accountant to file the P11d form at the end of the year.

What Can I do about it?

With an overdrawn director’s loan account there are limited remedies, and non that are pain free.

Here are a range of options

Repay the loan – if it’s under £10k you may be able to repay it then draw it back out shortly after – what is known as bed and breakfasting. This, however is not recommended as there are rules in place to combat it

Declare a “paper dividend” to clear the director’s loan account. This is where you declare a dividend, but pay no cash to yourself. The real sting in the tail is that, despite having not cash from the dividend, you will still need to pay dividend tax. You can only do this if you have sufficient “distributable reserves” to do so (basically profit not yet paid as a dividend).

Declare a bonus to clear the director’s loan account. This is the same as the above option for times where there are not sufficient distributable reserves. You will pay income tax, national insurance and the company will pay employers national insurance on this so its quite expensive.

Here are some things you can’t do

Ignore it – simply – that would be illegal (tax evasion, which once you do anything with it then becomes money laundering – all very serious)

Wind the company up – HMRC would have the right to object and appoint a liquidator. They would come after you personally for the money.

Director’s loans can get quite complex so its important to account for things well and get it right. Cloud accounting software can be a real help with this (FreeAgent is particularly good for this), as can having an accountant who is alert to this issue.

Ultimately, setting up your business in an efficient and structured way can help considerably to keep you organised. Simply being aware of the issue and avoiding making any large dividends at the end of the year often helps.

How to change your registered address when you’ve lost your Authentication Code

Your registered address for your company is your “official” address. It is where HMRC and Companies house will normally send their correspondence to. But what if you no longer have access to that address. It is quite common for people to register their address at their home, and then move house but forget to update Companies House.

If you have your Companies House Authentication Code it’s no big deal. You can go online and fill in the form AD01 online and the address is changed.

But what happens if you’ve lost the Companies House Authentication Code. The normal way to recover this code is to get Companies House to send it out to your registered address, but that is the reason you need to code in the first place.

In this situation, you have to go a bit old-school and send in a paper version of form AD01 to the following address:

The Registrar of Companies,

Companies House,

Crown Way,

Cardiff,

Wales,

CF14 3UZ

It normally takes a few weeks for the whole process to change. After that you can request that HMRC send out your Authentication Code, which takes another few weeks, at which point you have access to the company again.

Directors loan accounts. Use it, but don’t abuse it!

I was recently asked by a client whether he could take out a directors loan from his company, instead of drawing a salary or paying dividends. Its not an uncommon question and in fairness it’s something that did used to work. Sort of…

For those of you who don’t want the detail – let me be short.

NO – YOU CAN’T DO THIS AND YOU WILL GET STUNG FOR TAX IF YOU ATTEMPT IT. DON’T DO IT

There are essentially two facets to the question:

Do you get taxed personally

Does the company get taxed

Do you get taxed personally?

Essentially, if the company grants you personally a loan, without interest being paid, it is treated as a benefit in kind. Basically you are getting an economic benefit from the company, but not paying any tax on it. If this happens you pay income tax on the value of the benefit (which is actually the interest you would have paid if interest had been charged on the loan). The company also pays a type of national insurance called class 1a.

Under £10k, you are correct that the loan is treated as an exempt benefit. As a result there would be no income tax or company national insurance to pay.

Does the company get taxed?

This is the real mine field. There are two main issues here:

1 – Section 455 CTA 2010

Section 455, Corporation Tax Act 2010 is a key anti-avoidance weapon for owner-managed companies. Without it, owner managers could easily avoid a tax charge by arranging for ‘their’ company to lend them funds (as opposed to paying a ‘taxable’ bonus or dividend).

However, s455 levies a tax charge, equal to 32.5% of the loan, where a company makes a loan to you or one of your family members. In most cases, the s455 tax liability falls due nine months after the end of the accounting period in which the loan is made. The company is able to recover the s455 tax if and to the extent that the loans are repaid.

So basically – if the company loans you money, it gets charged tax on that loan as if it was a dividend at the higher rate. If you repay that loan you will get the tax back. If you never repay it you won’t. HMRC also charge you interest during this period and you can never reclaim it.

Under personal earnings of £100k there is no tax benefit, but much more work involved.

Some people have tried to get around this by paying back the loan and then drawing down another loan – this is what is known as “bed and breakfasting”. HMRC are all over this and have rules in place to stop this.

2 – Does the loan ever need to be repaid

Even if you decided that S455 was OK (not sure why you might, given it’s almost always a bad idea), essentially, eventually yes you do need to repay the loan in some way. When you come to wind up the company there will be an amount outstanding to you. To close down the company you will need to either

Repay the loan (getting back the tax levied, but not repaying the interest that HMRC charged)

Write off the loan (It will be treated then as income by HMRC – the type of income will be employment income and therefore you will, as well as needing to pay income tax, you will need to pay national insurance personal, and in the company)

Close the company in an insolvent state – you run the risk of a HMRC investigation with charges of fraudulent trading (which is a criminal offense)

There are lots of other tax rules that interact on winding up such as the Targeted Anti Avoidance rule (the so called anti-phoenixing rules) which further lock down this situation.

With the above in mind I would recommend against taking out a directors loan. You could loan yourself the money in the short term and then repay it using a dividend at the end of the year, but to be honest – you might as well just pay yourself a dividend in the first place and avoid the unnecessary loan step.

Does it ever work?

There is once circumstance where the S455 doesn’t apply and that is where the loan is under £5k, but you still have to think about how that loan will be repaid in the future.

One final thing is that the loan will also need to be disclosed in the accounts, which are on public record, but also with HMRC as well. I’m not sure if this is an issue for you. Personally it wouldn’t bother me but it’s something else to be aware of.

There’s no denying that directors loans are incredibly useful. Of course there are two sorts of directors loans. Loans where the director owes the company money – this is the subject of the above post.

The other, which is incredibly useful at times, is where the company owes the director.

Being able to generate a large directors loan account that the company owes you has potentially lots of benefits.

For starters you can charge interest on that loan. For basic rate tax payers you can receive up to £1,000 personally tax free. Meanwhile, your company can claim this cost against its corporation tax bill.

Furthermore, if you manage to arrange your affairs so that you have no taxable income from a salary, you can claim another £5k (note this doesn’t mean you can only get this if your earnings are nil, its just how you arrange things – we can help with this if you want).

Lets not forget – anytime you repay a loan to yourself, there is not income tax to pay on it.

Its about more than tax…

Directors’ loans are useful in the early stages of the business. I’m often asked what clients should do in terms of paying for things before they’ve had their first invoice paid. The answer is relatively easy

Pay for things yourself and keep a track of it (a bit of a pain admin wise)

Lend the company some money, and get the company to pay for it. Then have the company repay you later on when it has the funds.

The key point here is not to set up the company with lots of share capital (unless you need to for other reasons), which is what I find many clients thinking they need to do. A quick phone call to me tends to get them on the right track.

In summary

Don’t, if you can avoid it, try and pay less tax by loaning yourself money from a company – it doesn’t work – in fact it works out quite expensive.

You can borrow money in the short term, so long as you have a plan to pay it back. Keep on top of it though – don’t forget about it as it will catch up with you

Do think about directors loans from a tax planning perspective – particularly from a profit extraction perspective.

This needs to be completed at least once per year, even if your company is dormant.

If you don’t do this then Companies House can (and actually frequently do!) have your company struck off and effectively cease your assets, requiring you to undergo an administrative restoration to get your company, and all its assets back.

Don’t be late with this one – its easy and takes no time to do it

See how easy it is to file your confirmation statement online. Watch this short video and you’ll be guided through the steps.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

Manage consent

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.