“You’ve got to pay this amount of tax for the tax you owe.

And also this amount as well for the tax you might owe.

Oh and also you need to make another payment later for this.

Oh, by the way we then add it all up and then recalculated it, and then you will owe a different amount...”

If this is what your personal tax bills seem like, then panic not. Take a moment to get to grips with the initially seemingly confusing HMRC payments on account system for self assessments and bring understanding to the methodology behind the seeming madness!

What is the payments on account system supposed to do?

If you understand what HMRC are trying to do with the payments on account system, things might make a lot more sense.

The idea behind payments on account is to try to get you to pay your tax earlier. Not earlier than would be fair, but earlier than would be the case if they did nothing. By the time you make the tax payments, you should have already received the money that it relates to, meaning you should not be out of pocket.

How do individuals not on self assessment normally pay tax

Before we launch into this, its worth reminding yourself how employees paid through the payroll pay tax.

Each month or week their income is calculated, the tax deducted at source, and paid over to HMRC. Individuals should not ever get into tax issues with HMRC as it’s simply adjusted throughout the year. The amount of time between them earning the income any paying the tax is effectively nil.

If you are self employed, received dividends or rental income, or generally have a more complex tax position, where tax does not get deducted at source, things are a bit different. You will likely need to complete a self assessment tax return. Depending on the outcome of that return you may need to pay your tax bill using “payments on accounts”.

How Payments on Account works

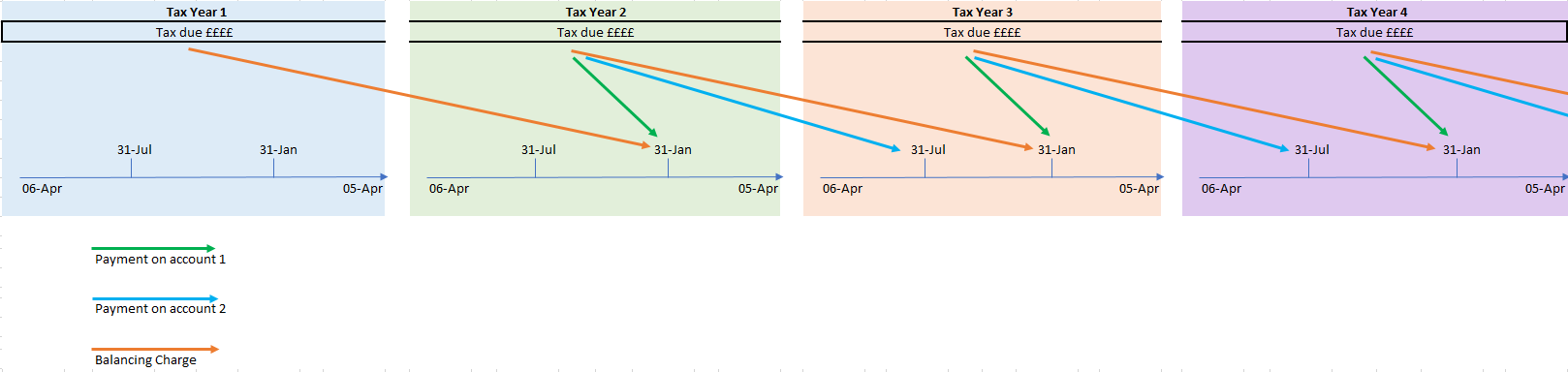

I’ve tried to explain this to clients using just words, and it doesn’t work -it really needs to be drawn out. So I’ve created an image to show you how it works below but I will also try to explain what you are looking at.

Payments on account are a way of paying you estimated tax for the year before you’ve actually submitted your tax return. It is based on an estimate, and is normally 50% of your pervious year’s income tax (and class 4 national insurance if you are self employed). It gets paid twice through the year – the 31st January and the 31st July.

Year 1 and the first payment on account

In year one, when you start, you earn all your money in that year, but don’t pay over the tax until the 31st January the following year. So if you started you business is April 2020, your first year end would be April 2021 and you wouldn’t pay tax on this income until January 2022 – that’s 21 months from April 2020! Compare that to being an employee where you have it deducted before you even receive it. HMRC would prefer it if you didn’t wait so long, and so they have this payments on account system to get you to pay over the money sooner

What many people consider to be the most painful part happens at the first payment date (see 31st Jan in year 2 below). You have all your tax to pay from year 1, plus 50% of the tax for year 2 (this is known as the 1st payment on account – green line). Most people consider this to be being taxed in advance, but do consider this which should help you feel better: You have already likely earned this profit by that point. Had you been an employee then you would have already paid over the tax. Now I appreciate that being in business etc is very different to being an employee, and that cashflow matters, but if you’ve been setting aside money to pay your tax bill as you go along, you should have already saved up this money.

So in your first year you tax payment (cash) might actually be 150% of your actual tax bill as a result!

Second payment on account

Then in the following July (blue line), you have another payment on account to make for the second 50%. At this point you will have paid 100% of your pervious year’s tax bill. As before, note that the timing of this means that you should have already received this income and it should not have caused a cashflow issue to you, if you have been saving up as you go along.

Balancing charge

Finally, you get to the next 31st January at which point you owe you “balancing charge”. This literally means calculating the difference between what you actually ended up owing in tax for the year, and deduct the two payments you have made throughout the year. If it is slightly more, you will owe HMRC some more money. If it is slightly less, you will technically be owed a refund (although see the next paragraph as to why you are unlikely to actually get a refund).

As well as the balancing charge, though, you also owe (you guessed it) the 50% first payment on account for the next year. So unless things have moved dramatically in the year, you are unlikely to actually receive any refund due as part of the balancing charge at this point.

If things have not moved that much you then enter into a period where you pay 50% of your bill in January, 50% of your bill in July and then pay a balancing adjustment in the following January

Self-Assessment – when payments on account kicks in

The payments on account system automatically kicks in unless

- your last Self Assessment tax bill was less than £1,000

- you’ve already paid more than 80% of all the tax you owe, for example through your tax code or because your bank has already deducted interest on your savings

So, many people will be caught by this.

Final thoughts

The payments on account system is, at first, really confusing, particularly in the first year. It’s really important that you budget for the tax you are going to pay throughout the year so you have cash saved up ready for these payments as they come up. Despite how it may look and feel, you are not paying tax in advance of your generating profits, but more in advance of you filing the tax return.

Obviously, there is the possibility that your payments on account are too much, if in the current year you earn less than the previous year. HMRC provide a mechanism for adjusting the amounts provided you have a reasonable justification. We’ve found them to be quite pragmatic in the past with this.