‘Tis the season to be jolly! With the holiday season right around the corner, businesses everywhere are getting ready to throw their annual work Christmas parties. These festive shindigs are not only a chance for colleagues to come together and let loose, but they also have some financial implications that we need to talk about. So grab your Santa hat and let’s dive into the world of tax deductions and festive fun!

There are three main things to consider.

The tax deductibility of the party for your business

The impact on your staff and their taxes

The VAT you can reclaim

Tax-deductibility of Work Christmas Parties

Let’s talk about the tax-deductibility of work Christmas parties. It’s actually a pretty nifty opportunity for businesses to save some cash.

But there is a catch!

When it comes to claiming tax deductions, businesses need to be careful. They can only deduct expenses for entertaining their lovely staff members (as in actual employees), not for non-staff folks like customers and suppliers (which, for the record includes contractors and freelancers – as they are not employees). So, keep that in mind when you’re tallying up the costs.

That’s not to say don’t entertain your customers and suppliers, but just be aware that its not tax deductible.

Taxable Benefit for Staff Attending

Its worth being aware that as well as the tax situation for your company, you should also consider the impact on your staff’s tax. Afterall, nobody is going to thank you for providing them with a killer party, only later to be hit with an unexpected tax bill.

First off, if the main purpose of the event is to entertain employees, then it’s usually tax-free. So get ready to deck the halls and have a jolly good time!

The party must be an annual thing, planned in advance, and open to all employees. Also, it can’t cost more than £150 per person. That means you can’t go all out and hire Mariah Carey to sing at the party.

If your company has different locations or departments, it’s fine to have separate parties, as long as all employees have the chance to attend at least one of them.

But here’s the catch: if the cost per person exceeds £150, the whole shebang becomes taxable. So be careful not to go overboard with the eggnog and caviar.

Bringing Guests

Oh, and one more thing: your staff members can bring along a plus one, but their costs must be included within the £150 limit. So if they want to bring their partner or their cousin’s best friend’s dog, it’s on them to make it work within the budget.

These conditions are here to make sure that staff entertainment stays tax-free and everyone has a holly jolly time. So it’s crucial for businesses to understand the tax implications and follow the rules. Trust us, you don’t want to end up on the naughty list of penalties and extra tax charges.

The £150 Threshold

If the total cost of your event goes over £150 per person, it becomes a taxable benefit.

You need to be clear that the £150 is not an allowance, its an exemption – under £150 per person and it’s exempt. Over £150 per person, the whole amount is taxable.

Yup, you read that right. The taxman wants a piece of the pie. And don’t forget to factor in the cost of your staff members’ partners or guests. They count too and need to be included in that £150 limit per head.

This limit includes everything you can think of when it comes to event costs – the food, drinks, entertainment, accommodation, and even transport. So, if you’re hosting a mixed event with both staff and non-staff attendees, you need to do some math to figure out the cost apportionment.

It also, it’s worth saying, includes other staff entertaining from the year, so if you have both a summer and and Christmas partythe limit takes into account both those parties – in other words – it’s per year, not per event!

To avoid any unwanted penalties and extra tax charges, it’s crucial to keep track of all your event expenses. Be a good bean counter and record everything accurately. By staying within that £150 threshold, you can keep your event tax-deductible and minimise any financial impact on both your company and your beloved employees.

So, go ahead and plan that amazing Christmas party, just make sure you stay within the boundaries. After all, nobody wants their festive cheer to turn into a tax nightmare.

Exemption Conditions Not Met

Hey there! So, let’s talk about work Christmas parties and what happens when they don’t meet the exemption conditions. Brace yourself, because things can get a little… taxable.

Yep, you heard me right. If these parties don’t meet the exemption conditions, they become a taxable benefit that needs to be reported on form P11D. And trust me, nobody wants to deal with penalties for non-compliance.

Now, I don’t want to scare you, but it’s important to stress the need for accurate record-keeping. Seriously, it’s like the holy grail of avoiding issues and penalties. So, here are five key points you should keep in mind:

Don’t go overboard! If you incorrectly claim the exemption or exceed the £150 per head limit, you might end up facing penalties and extra tax charges. Nobody wants that, right?

Keep those records in check! You need to have accurate records of all the costs involved in the event. Invoices, receipts, the whole shebang. This way, you can prove that everything is above board and avoid any unnecessary drama.

Taxes, taxes, taxes! When it comes to the taxable benefit, the employee is the one who needs to pay up for the tax and National Insurance Contributions (NICs). But hey, if the employer is feeling generous, they can also settle the bill via a PAYE settlement agreement.

Non-compliance is a no-no! Not following the exemption conditions can have some serious financial consequences. And I’m not just talking about the employees here. Employers can get hit with some hefty penalties too.

Follow the guidelines and stay on top of those records! It’s super important to make sure you’re complying with all the rules and regulations. Trust me, it’s the best way to avoid any unnecessary penalties and keep everyone happy.

VAT on Christmas Parties

If your business is registered for VAT, there’s even more good news. You might be able to reclaim some, or possibly all the VAT you paid for hosting the Christmas party.

Now, before you start picturing yourself swimming in a pool of reclaimed VAT, let me break it down for you. Reclaiming VAT involves keeping accurate records and following those VAT rules and regulations. If your business is registered for VAT, there’s a chance you can reclaim the VAT on your party costs. But remember, you got to follow the right procedures and do everything by the book.

So, let’s get into the nitty-gritty. Here’s a handy-dandy table to help you understand the impact of VAT on your party costs:

VAT on Party Costs

Impact

Non-staff entertaining

You can’t normally claim this.

Staff entertaining

You may be able to claim the VAT back on this – see the conditions below

The conditions for claiming VAT back on staff entertaining are:

Entertainment should be provided to employees as a way to reward them for their good work or to improve staff morale.

Entertainment should not be provided exclusively to directors, partners, or sole proprietors.

Employees should not be responsible for hosting non-employees during the entertainment.

All these conditions must be met in order to make the claim. If any are not then you can’t claim this.

It’s worth saying that the broader question over claiming VAT on entertaining is a complex area so, as so often is the case, there is a certain amount of “it depends” but the above gives you the broad strokes of what you can and can’t claim.

By reclaiming VAT, you can lighten the financial load of hosting a Christmas party and make sure you’re taking full advantage of those tax benefits. But hold your horses, my friend – it’s important to consult a tax professional or refer to the guidelines to ensure you’re compliant with all the VAT regulations. And don’t forget to keep track of your expenses and reclaim VAT accurately.

Conclusion

It’s important for businesses to understand the tax implications so they can navigate the complexities and stay on the right side of the law. After all, nobody wants to deal with unnecessary financial consequences, especially during the festive season!

By making the most of deductions and meeting all the necessary criteria, businesses can minimize those pesky financial burdens and really get into the holiday spirit. So, while you’re out there spreading the festive cheer, keep in mind the importance of accurate record-keeping and VAT compliance. Trust me, it’ll come in handy when you need to reclaim VAT on those party costs.

Now, go ahead and unleash the festive fun, but remember to stay informed and make wise tax choices. It’ll keep your business in good standing and ensure you can enjoy all the merry celebrations without any additional headaches.

If you’re in the mind to shower business gifts on your suppliers, employees or customers, it’s critical that you understand that tax implications of what you are doing.

By sticking with to the guidelines set by HMRC, you can make sure that you handle them correctly.

As always, it is recommended to consult with a qualified accountant (like us) for specific advice for your personal circumstances.

Have you ever wondered what qualifies for deduction? We will cover that for you. We will also explain the conditions that need to be met in order for a gift to be tax deductible. And don’t forget about the VAT considerations! We will break it down so you can understand how VAT applies to your business gifts.

At The Accounting Studio, we understand the importance of compliance with HMRC regulations. Our accountancy packages include accounting support and quick queries, so you are always just a call or email away from quality advice.

With our expertise and dedication to accessibility in accountancy, we are here to guide you through the complexities of tax deductibility for business gifts.

Key Points

Corporate gifts are typically not eligible for tax relief.

However, there are exceptions for items given away for advertising purposes, as long as their value is less than £50.

The combined value of multiple gifts given to the same recipient should not exceed £50 in a single accounting period.

Gifts given to employees can be deducted in company accounts, and VAT can be reclaimed.

Overview of Business Gifts

When it comes to giving gifts in a business context, it is important to understand the rules surrounding tax deductibility. In the UK, there are specific guidelines that determine whether a business gift can be deducted as a legitimate expense.

First and foremost, it is crucial to note that HM Revenue and Customs (HMRC) has set limits on the value of gifts that can be claimed as a tax deduction. According to these guidelines, a business can deduct up to £50 per gift for its clients or customers. However, this deduction is subject to certain conditions.

To qualify for tax deductibility, the gift must meet a few criteria. Firstly, it should be given to a client or customer, and not to employees or suppliers. Additionally, the gift should be given with the purpose of promoting the business or fostering goodwill. If these conditions are met, the cost of the gift can be claimed as a deductible expense.

It is important to note that gifts with a value exceeding £50 cannot be claimed as a tax deduction, regardless of the circumstances. In such cases, the full cost of the gift will be considered a non-deductible expense.

Also, it is advisable to keep proper records and documentation of all business gifts. This includes details such as the recipient’s name, the occasion, the cost of the gift, and the purpose for giving it. These records will be necessary in case of an HMRC audit or when filing tax returns.

What qualifies for deduction?

If you want to know what qualifies for deduction when it comes to business gifts, The Accounting Studio provides a guide that explains the criteria.

Tax deductible items are those that can be claimed as an expense and reduce your taxable income. However, when it comes to business gifts, they are not normally eligible for tax relief. There are exceptions for items given away for advertising purposes with a value of less than £50.

It is important to note that the total value of multiple gifts to the same recipient should be less than £50 in one accounting period. Additionally, if the value of the gift or gifts is more than £50, VAT needs to be accounted for, unless it is a business sample.

Gifts to employees, on the other hand, are deductible in company accounts and VAT can be reclaimed.

Conditions for deductibility

In order for an expense to be deductible, it must meet certain conditions. These conditions vary depending on the type of expense and the jurisdiction. However, there are some general requirements that apply in most cases.

Firstly, the expense must be incurred in the course of carrying on a trade, business, or profession. This means that the expense must be directly related to the activities of the business and necessary for its operation.

Secondly, the expense must be incurred for the purpose of generating income or profits. It must not be a personal or private expense unrelated to the business. For example, the cost of entertaining clients may be deductible if it is directly related to the business and incurred for the purpose of generating income.

Thirdly, the expense must be supported by proper documentation. This includes invoices, receipts, and other records that provide evidence of the expense and its business purpose. Without proper documentation, the expense may not be deductible.

Finally, the expense must comply with any specific rules or limitations set out in the tax laws. For example, there may be limits on the amount of certain types of expenses that can be deducted, or certain expenses may be disallowed altogether.

It is important to consult with a tax professional or refer to the specific tax laws in your jurisdiction to determine the exact conditions for deductibility.

To be eligible for deduction, ensure that the value of the gifts given to the same recipient does not exceed £50 in one accounting period. It is important to comply with HMRC regulations to ensure the deductibility of business gifts. To help you understand the requirements, refer to the table below:

Deductibility Requirements

HMRC Regulations

Gift value ≤ £50

Yes

Gift value > £50

VAT accounted for

Gifts for advertising purposes

Yes, if value ≤ £50

Gifts to employees

Deductible in company accounts

VAT reclaimable

Yes, for gifts to employees

By following these deductibility requirements and adhering to HMRC regulations, you can ensure that your business gifts are eligible for tax deduction.

VAT considerations

Consider the VAT implications when giving away items of value, as exceeding the £50 limit may require you to account for VAT, unless it’s a business sample.

It’s crucial to understand the impact on gift recipients and the importance of accurate record keeping.

Failure to account for VAT correctly can result in penalties and non-compliance with HMRC regulations.

To ensure compliance, keep a detailed record of all gifts given, including their value and recipient.

This will help you accurately calculate the VAT owed and avoid any potential issues.

Accurate record keeping also allows you to demonstrate the legitimacy of your gifts and their advertising purposes, which may qualify for tax relief.

Therefore, it’s essential to maintain meticulous records to support your tax deductibility claims and avoid any misunderstandings with HMRC.

If you are a limited company owner looking to reduce your tax liability and increase your take home pay, this article is for you. By following these tips, you can save money and maximise your profits.

Tax-Efficient Remuneration

If you are a limited company owner operating outside of IR35, you have more control and flexibility over your remuneration. By structuring your payments through a combination of salary and dividends, you can reduce your income tax and National Insurance contributions, resulting in more take home pay. Dividends are company profits distributed among shareholders, so if you are the only shareholder, the dividends are all yours!

It is important, however, not to withdraw all your company profits as dividends. Keeping some money in your business will provide flexibility in case your business faces a lean spell. Also, retaining funds in the business can help you to pay less tax as it could keep you in a lower tax band.

Give Gifts to Charity

Making donations to charity, such as money, shares, property, equipment or land, can reduce the amount of corporation tax you pay. The value of the donations is deducted from company profits before tax is applied. Donations can be made through personal contributions or Gift Aid. This tax relief is available to sole traders, partnerships and limited companies, but the rules are slightly different for limited companies.

Utilise the Flat Rate VAT Scheme

Many self-employed people operating outside IR35 use the Flat Rate VAT scheme to simplify the process of charging and reclaiming VAT. This scheme removes part of the administrative burden associated with being VAT registered. Through the flat rate scheme, a fixed rate of VAT is paid to HMRC and you keep the difference between what you charge your customers and what you pay HMRC. VAT can’t be reclaimed on purchases with the exception of specific capital assets over £2,000.

The flat rate VAT percentage you pay is dependent on the sector your business operates in and the cost of goods used. If you’re in your first year as a VAT-registered business, you will get a 1% discount. To be eligible for the scheme, your VAT taxable turnover must be less than £150k, your business cannot be closely associated with another business, and you cannot have been found guilty of a VAT offence, or paid a penalty for VAT evasion, within the last year.

Use Your ISA Allowance

You can use an ISA to reduce your tax bill . Each year you can put up to £20,000 into it. This could be all in one ISA or split between a cash ISA, stocks & shares ISA, innovative finance ISA or a lifetime ISA. If you earn interest from a cash ISA it’s not subject to income tax, so it is tax-free. You also don’t have to pay tax on any dividends received or capital gains realised from shares held in a stocks & shares ISA.

Make Contributions To Your Pension

Pension contributions are an allowable expense that can lower the amount of corporation tax you pay. As a limited company owner, you can make contributions to your pension to trim the amount of tax you pay. This will enable you to lower your corporation tax liability and increase your take home pay.

Work with an accountant that’s right for you

Looking for more ways to pay less tax? Working with an accountant is a smart move.

At The Accounting Studio, we specialize in accounting for small businesses and the self-employed. Our expert accountants can help you reduce your tax liability and handle all the necessary documentation for HMRC. We know how to maximize your profits so that you’re only paying the amount of tax you should be paying to HMRC, and not a penny more.

Our transparent fixed-fee pricing structure ensures that there are no unpleasant surprises. You’ll have your own dedicated accountant, full access to the market-leading FreeAgent accounting software, and a same-day response to any query submitted on a working day before 3pm.

By paying a monthly fee, you’ll gain access to our expertise and get the best advice on how to leverage all available tax efficiencies, ultimately increasing your take-home pay. Plus, you’ll save a ton of time by not having to handle your accounts and record-keeping yourself. Instead, you can focus on growing your business.

Remember, working with The Accounting Studio means having an expert in your corner, helping you to keep more of what you earn and grow your business.

Conclusion

Incorporating your business can bring many benefits, including limited liability, credibility, and the ability to claim a wider range of expenses. To maximise your take home pay, consider structuring your remuneration through a combination of salary and dividends, making donations to charity, using the Flat Rate VAT scheme, taking advantage of your ISA allowance, and making contributions to your pension. By following these tips, you can reduce your tax liability and increase your profits. At The Accounting Studio, we are always ready to help.

You would be forgiven for thinking that, given all the tax changes that have happened in the year, including the change in corporation tax rate coming into effect for 2023/24, that there would be more in the way of changes for dividend vs salary.

Well here at The Accounting Studio, we have spend a not inconsiderable amount of time crunching the numbers, running over 2000 scenarios and poring over the data, only to find that the recommendations from last year, pretty much hold for this year as well.

One of the most fundamental ways for company owners to manage (minimise!) their tax liability is by making sure they are using the most appropriate split between dividend vs salary 2023/24.

There are a myriad of ways that this can be done and each individual will need to take into account their particular personal taxation circumstances. Sometimes what appears to be the most tax efficient way to extract funds stands in stark contrast with another personal objective – usually getting a mortgage. So before diving in and ruthlessly efficiently managing your tax liability, pause for thought about what other impacts this might have. Talk to a mortgage advisor if necessary to find out what income, and of what type, you may need in order to secure that mortgage that will buy you that dream (or maybe first) property.

Assuming that paying as little tax as is legal is the aim of the game – read on…

First – a bit of background on the two items

What is a dividend

We’ve written more on this in our guide to dividends, but to save you the effort of clicking on the link and reading this splendid exposition the short version is that it is

The payment of profits to shareholders (note that’s shareholders, not directors)

You can only pay dividends if you have profits to pay out (bare in mind this is after corporation tax – don’t forget to account for that)

Normally paid in proportion to the shares held (so if there are two shareholders, “Barry” owning 70% and “Cecily” owning 30% and you pay a £10k dividend, Barry should receive £7k and Cecily should receive £3k

They need to be approved and declared correctly

Dividends are paid after corporation tax, meaning they are not themselves a tax deductible expense.

If there are insufficient profits then it the money you pay out would likely be classed as a director’s loan that you would have to repay, and on which all sorts of tax complications arise

Dividends have a lower income tax rate than salary and are not subject to national insurance contributions

What is salary

Sounds stupid, right? But let me be clear as this has caught out more businesses that I’ve come across that it has any reason to:

Salary is money paid that has been processed through PAYE and reported to HMRC. If you’ve not reported it through PAYE it’s not salary – OK!

What that means is registering the company as an employer and making monthly “Real-time-information” (RTI) submissions using payroll software.

The Aim

Usually there are a few aims

Take as much salary as possible without paying income tax. This is because it is a tax deductible expense.

Avoid having to pay employers national insurance contributions, so long as that is beneficial

Have the salary set so that it counts towards your national insurance record, hence protecting your rights to state benefits (such as state pension)

Changes this year

Company changes

The key change for companies is the change in rate of corporation tax from 19% to 25%. The change is very complex, but the simple version is this:

Assuming you have no associated companies (more on this later), your company will be taxed as follows, and your company is not receiving any dividend income from non-group companies:

Profits up to £50k are taxed at 19%.

Profits between £50k and £250k are taxed at a marginal rate of 26.5%

Profits above £250k are taxed at 25%

The net effect of this, particularly the middle band, is that by the time you are generating £250k in profits, your whole profit will be being taxed at 25%.

This is only in effect from 1st April 2023. So if your year end is, say, June 2023 this whole arrangement (for this year only) will adjusted so that 3/12ths of your profits will taxed under this new regime, but the bands will then also be adjusted to 3/12ths.

So for your first year it will only partly affect your tax, then in future years it will apply for the whole year going forward.

Complex you say? Yes, says I!

But we haven’t even got started…

Associated Companies

There are a range of extremely complicated rules that come along with this that change the band thresholds based on a number of different circumstances.

One of the ways that these bands will change is whether there are any “associated companies”. If you have one associated company then the Small Company Rate band halves to £25,000, and if you have two associated companies then it reduces to £16,666,66 (i.e. it divides by three – the two associated companies plus the company in question).

In effect the Small Companies Rate band is shared between the associated companies.

The same is true of the main rate band of £250,000.

For this reason it is an essential requirement that we correctly identify all your associated companies. The legislation casts the net very wide.

Associated companies are any companies where one is controlled by another, or both are controlled by one, or a number of individuals or companies.

Associates also takes into account your family’s businesses where there is also “substantial commercial interdependence“, which is a whole other level of complexity, but could mean that because you loaned some money to your children’s/parent’s/brother’s/sister’s company, or you have customers in common with them, your tax rate may change.

The rules are somewhat berserk, but they still exist, and therefore need to be treated with the sort of respect you give when stumbling across a hungry bear in the forest: You don’t have to like it, but you do need to acknowledge that its there, and if you make a wrong move, it might just rip your head off.

Income Tax

Dividend tax rates

Last year the rate at which dividends went up in line with National Insurance to pay for the Health and Social Care bill. Without rehashing all the excitement that happened this year with taxes and budgets, the final outcome is that the 1.25% increase on National Insurance has now been reversed, but the increase on dividends still remains.

Dividend tax rates remain therefore the same as 2022/23

Tax band

2023-24

2022-23

Basic rate

8.75%

8.75%

Higher rate

33.75%

33.75%

Additional rate

39.35%

39.35%

There is also a band change that needs to be considered for individuals. The threshold at which the additional rate of tax applies has been reduced from £150k to £125,140

Tax band

Band 2023/24

Band 2022/23

Basic rate

£12571 to £50270

£12571 to £50270

Higher rate

£50271 to £125,140

£50271 to £150,000

Additional rate

£125,140 +

£150,001 +

Dividend allowance

In the 2022/23 you would be eligible to receive £2,000 of dividends at nil tax. This is being reduced in 2023/24 to £1,000

Optimal Salary 2023/24

Despite all the changes and complications of the change in corporation tax, I have run the numbers (over 2000 scenarios), and the conclusion I have drawn is that the recommendations in terms of salary for this year actually remains the same as in the previous year, and the same three options available to you last year are the same options this year (I was expecting something different but the calculations prove otherwise).

So the optimal salary, as we have crunched the number, for most directors who are taking both a salary and dividends, is……

£11,908 per annum

£993.44 per month

At this level you will be paying employers national insurance and this is why we are urging caution to clients who have not historically paid this.

You will need to remember to actually pay it.

It will not take much in the way of fines to nullify the tax savings you make at this level – so if you are organised and trust yourself to be on top of your admin, you should be fine. If you are already running a payroll and making regular payments to HMRC, again you should be fine.

But for those single director companies who don’t have this monthly process currently, it could be an issue.

If you are perhaps a bit more, err, free spirited (?!), the next option is what we are recommending

Safest Dividend vs Salary 2023/2024

If you are not 100% certain that you will be able to make sure that the correct payments get made to HMRC for payroll on time, every time, you should consider this option:

You should look to be paying yourself £758.33 per month in salary. At this level you will be contributing to your state pension but not actually paying any income tax or national insurance. You also won’t have to (normally) make payments over to HMRC at regular intervals, and so is administratively far less of a burden, and far less likely to incur fines as a result.

Optimal Dividend vs salary 2023/24

Due to the enhance complexity in the tax system at the moment, rather than give you single figure for what your tax efficient dividends would be this year, I need to give you a method for working it out yourself.

The most tax efficient dividends you take throughout the year will depend on a few things:

Your salary (see above)

Your residential property income

Your other taxable income

Whether you, or your partner, receives child benefit

Here is the rule of thumb for you

Work out your higher rate threshold

If you or your partner are receiving child benefit, and your partner earns less than £50,000, your higher rate threshold is £50,000

If you or your partner are not receiving child benefit, your higher rate threshold is £50,270

Deduct from this the total salary you will receive in the year (see above)

Deduct from this the expected profit from residential properties in the year EXCLUDING mortgage interest

Deduct other expected income in the year (e.g. other salaries, benefits in kind received, income from self-employment, interest, other dividends, other property income etc)

If the figure is still positive, this is the most tax efficient dividend you can take.

Obviously, the normal rules apply for dividends – they are paid out of post corporation tax profits and need to be properly authorised (profit assessment/board minutes/dividend vouchers etc). You need to have sufficient profits in the business to be able to pay these dividends. If you don’t have sufficient profits, it will be treated as a director’s loan which has lots of complicated tax consequences.

Final thoughts

So the advice for dividend vs salary 2023/24 this year is a bit more complicated than in previous years. Obviously, the above is meant to inform you rather than provide you with specific advice personal to your own circumstances.

If you feel like you need a more tailored approach we would be delighted to have a chat with you to find out how we could help. Tax really is quite complicated, and is getting more so. Don’t rely on what is generic information above – talk to a professional to make sure you are making the right decision when it comes to extracting profit from your business in a tax efficient way and working out what the most effective dividend vs salary 2023/24 for you.

“You’ve got to pay this amount of tax for the tax you owe. And also this amount as well for the tax you might owe. Oh and also you need to make another payment later for this. Oh, by the way we then add it all up and then recalculated it, and then you will owe a different amount...”

If this is what your personal tax bills seem like, then panic not. Take a moment to get to grips with the initially seemingly confusing HMRC payments on account system for self assessments and bring understanding to the methodology behind the seeming madness!

What is the payments on account system supposed to do?

If you understand what HMRC are trying to do with the payments on account system, things might make a lot more sense.

The idea behind payments on account is to try to get you to pay your tax earlier. Not earlier than would be fair, but earlier than would be the case if they did nothing. By the time you make the tax payments, you should have already received the money that it relates to, meaning you should not be out of pocket.

How do individuals not on self assessment normally pay tax

Before we launch into this, its worth reminding yourself how employees paid through the payroll pay tax.

Each month or week their income is calculated, the tax deducted at source, and paid over to HMRC. Individuals should not ever get into tax issues with HMRC as it’s simply adjusted throughout the year. The amount of time between them earning the income any paying the tax is effectively nil.

If you are self employed, received dividends or rental income, or generally have a more complex tax position, where tax does not get deducted at source, things are a bit different. You will likely need to complete a self assessment tax return. Depending on the outcome of that return you may need to pay your tax bill using “payments on accounts”.

How Payments on Account works

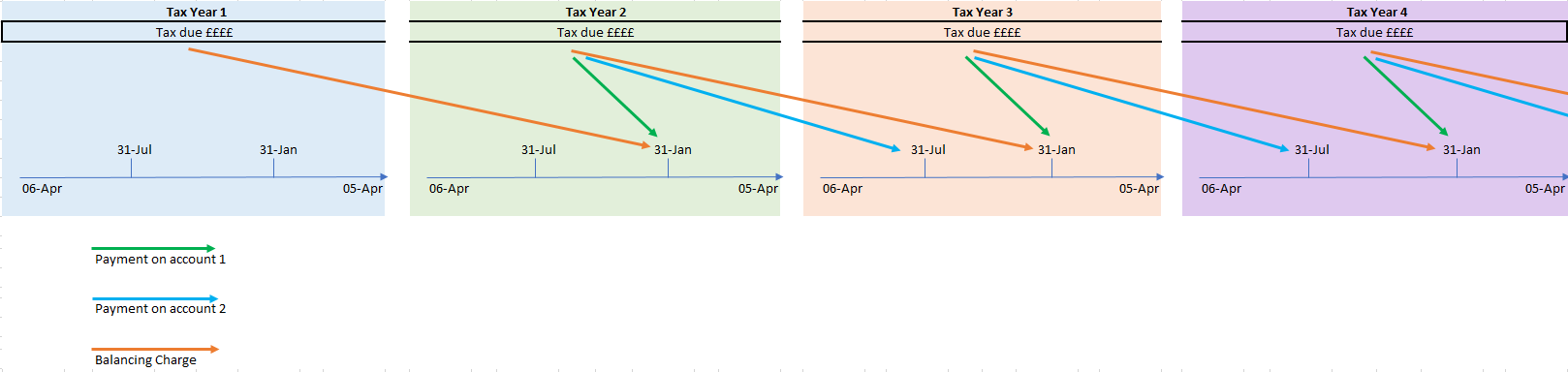

I’ve tried to explain this to clients using just words, and it doesn’t work -it really needs to be drawn out. So I’ve created an image to show you how it works below but I will also try to explain what you are looking at.

Payments on account are a way of paying you estimated tax for the year before you’ve actually submitted your tax return. It is based on an estimate, and is normally 50% of your pervious year’s income tax (and class 4 national insurance if you are self employed). It gets paid twice through the year – the 31st January and the 31st July.

Year 1 and the first payment on account

In year one, when you start, you earn all your money in that year, but don’t pay over the tax until the 31st January the following year. So if you started you business is April 2020, your first year end would be April 2021 and you wouldn’t pay tax on this income until January 2022 – that’s 21 months from April 2020! Compare that to being an employee where you have it deducted before you even receive it. HMRC would prefer it if you didn’t wait so long, and so they have this payments on account system to get you to pay over the money sooner

What many people consider to be the most painful part happens at the first payment date (see 31st Jan in year 2 below). You have all your tax to pay from year 1, plus 50% of the tax for year 2 (this is known as the 1st payment on account – green line). Most people consider this to be being taxed in advance, but do consider this which should help you feel better: You have already likely earned this profit by that point. Had you been an employee then you would have already paid over the tax. Now I appreciate that being in business etc is very different to being an employee, and that cashflow matters, but if you’ve been setting aside money to pay your tax bill as you go along, you should have already saved up this money.

So in your first year you tax payment (cash) might actually be 150% of your actual tax bill as a result!

Second payment on account

Then in the following July (blue line), you have another payment on account to make for the second 50%. At this point you will have paid 100% of your pervious year’s tax bill. As before, note that the timing of this means that you should have already received this income and it should not have caused a cashflow issue to you, if you have been saving up as you go along.

Balancing charge

Finally, you get to the next 31st January at which point you owe you “balancing charge”. This literally means calculating the difference between what you actually ended up owing in tax for the year, and deduct the two payments you have made throughout the year. If it is slightly more, you will owe HMRC some more money. If it is slightly less, you will technically be owed a refund (although see the next paragraph as to why you are unlikely to actually get a refund).

As well as the balancing charge, though, you also owe (you guessed it) the 50% first payment on account for the next year. So unless things have moved dramatically in the year, you are unlikely to actually receive any refund due as part of the balancing charge at this point.

If things have not moved that much you then enter into a period where you pay 50% of your bill in January, 50% of your bill in July and then pay a balancing adjustment in the following January

Self-Assessment – when payments on account kicks in

The payments on account system automatically kicks in unless

your last Self Assessment tax bill was less than £1,000

you’ve already paid more than 80% of all the tax you owe, for example through your tax code or because your bank has already deducted interest on your savings

So, many people will be caught by this.

Final thoughts

The payments on account system is, at first, really confusing, particularly in the first year. It’s really important that you budget for the tax you are going to pay throughout the year so you have cash saved up ready for these payments as they come up. Despite how it may look and feel, you are not paying tax in advance of your generating profits, but more in advance of you filing the tax return.

Obviously, there is the possibility that your payments on account are too much, if in the current year you earn less than the previous year. HMRC provide a mechanism for adjusting the amounts provided you have a reasonable justification. We’ve found them to be quite pragmatic in the past with this.

For parents receiving child benefit, particularly those that have investment properties, or have earnings from a company, you really need to read this to avoid a large potentially avoidable sneaky tax charge – the High Income Child Benefit Tax. This is known as the £50k child benefit trap.

The government brought in a tax measure several years ago to ensure that families who are “high earners” do not ultimately receive it.

The mechanism they settled on to ensure that the “better off” don’t receive this somewhat meagre hand out is fairly complex. Many parents are aware of this but in case you are not here is a brief summary

The High Income Child Benefit Charge

HMRC decided that, rather than simply not give you the child benefit in the first place, it would be far better to give you the benefit, and then basically claw it back if you earn more than they deem to be enough.

So you get the child benefit throughout the year, in the normal way.

Then at the end of the year, when

you complete your tax return and tell HMRC that you have received child benefit (one rather suspects that they already know this!); and

if you’ve earned above the threshold, pay some or all of it back to HMRC through your self assessment tax payments

This tax charge is called the “High Earner Child Benefit Charge”.

Now, it’s important to be aware that this tax is assessed on both “parents”. I say “parents” as its really based on adult child carers in the household. And the thinking behind it is pretty weird…

How does the High Income Child Benefit Charge work in practice?

The tax charge applies only to the higher earner and it works like this.

Up to £50k income there is no tax charge.

Above £50k HMRC claws back 1% of everything you have received for child benefit in the year for each additional £100 you earn.

So if you earned £55,000 you would owe half (50%) of what you had received in child benefit in the year. If you had earned £56,000 you would owe back 60% of what you owed in the year.

This continues up to an income of £60k, where at that point you would have repaid all the child benefit.

Do bare in mind that if one of you earns £60k and the other earns nothing, all the child benefit gets repaid. On the other hand, if you both earn £50k (so a household income of £100k – far better off than the single earner bringing in £60k), no child benefit is clawed back. Not, it would seem, a very well targeted tax given the hoops that need to be jumped through.

But this isn’t really the trap I was talking about – not the main trap – this is just the plain vanilla trap to be aware of.

What counts as earnings?

The real trap comes into play once you start looking at what is treated as “earnings”. This is not just your salary, it’s all you taxable earnings, which includes dividends, benefits in kind, interest, and most devastatingly rental income.

Historically, with property income you would calculate your profits net of mortgage interest, however recent changes (for residential buy to let landlords at least) has changed that.

I won’t go into the detail of how the changes work but a brief overview is that when calculating what your property income is, for residential buy to let properties, you now completely exclude the mortgage interest.

So as an example – where you previously earned rental income of £20k, with costs of £4k and mortgage interest of, say, £13k, you property income for tax purposes would be £3k, and you would be taxed on that £3k (£20k less £4k less £13k).

Why does this matter? The £50k child benefit trap

Using the example above, this £3k would previously have been treated as “income” when calculating how much you had earned for child benefit purposes. This meant that so long as you earned £47k or less for all your other income sources, you would not be paying the higher income child benefit charge

Now, things have changed. Using the above example, your property income would be treated as being £16k (£20k rental income less 4k costs – no account taken of your mortgage interest), and it is here where the trap lies.

With your property taxable income going up from £3k to £16k, now you can only earn (using the above example) £34k before the high income child benefit charge kicks in. If you maintained you income at £47k your taxable income would actually be £63k, meaning you would owe ALL the child benefit you received in the year back which could be a substantial amount.

Avoiding the £50k child benefit trap?

There are relatively limited measures you can take to avoid this additional tax charge but here is my list of a few favourites

If you are earning above £50k and below £60k

Pay into a pension scheme personally. Doing this reduces you taxable income and therefore reduces your high income child benefit charge. Its tax effective in that you save yourself 40% income tax, plus save yourself the child benefit tax. You get to keep the money, although you can’t use it until you draw your pension.

Give personally to charity – this works the same as for pensions, only you end up with a warm fuzzy feeling, rather than money in your pension pot.

For people earning income from their company through dividends

Consider taking less in dividends. If your lifestyle does not require it, adjust your dividends so that you do not “earn” over £50k

If you are married and your spouse earns less than £50k, consider making your partner a shareholder. This is complex from a tax perspective and needs to be done right so you should take expert advice (…happy to help…) on

the transferring of shares to avoid triggering capital gains tax

considering whether different classes of shares are required to pay different dividends

For everyone

Consider whether it is worth transferring you property into a limited company so that you can control what earnings are taxed on you personally, and when.

Conclusion

Ultimately you need to sit down with your accountant early in the tax year and decide on a strategy to deal with this, if its something that is going to be an issue for you. You have some options, but its not the same as it was a few years ago before the new rules on residential mortgage interest were brought in.

We often get asked by clients about what whether there are tax free benefits that they can be getting from their company: Benefits they can receive without paying tax on them.

Here is our list of the top 8 benefits that you can provide to employees and directors of your company.

Normally, when you provide a benefit to your staff (or to you if you a director of the company), both the staff and the company are taxed on that benefit. There are some benefits where you don’t pay tax. In fact, better than that, the costs are tax deductible in the company.

You can get up to £300 for trivial benefits from the company, up to £50 in each instance, each year.

3. Mobile phone

The company can provide you with a mobile phone tax free. There are, however, some critical conditions – one of which is that the contract must be in the company name. If the contract is still in your name then it is simply treated as extra salary, which is expensive from a tax perspective.

4. Christmas or annual party

You can spend up to £150 (including VAT) per person for a Christmas party as a tax exempt benefit. Note that is “up to” – a single penny more and the whole lot becomes a benefit in kind and taxable on both you and the company. Typically you would not be able to recover any VAT suffered on the costs.

5. Counselling

It’s great to know that counselling is a tax-exempt benefit. So if you are having a hard time, and need to see someone about your mental health, your company can foot the bill.

This also includes couples counselling but does not include medical, financial, legal or recreational counselling (so you can’t call your personally trainer your fitness counsellor!)

6. Home working allowance

If you work from home you can claim up to £6 per week as a contribution towards additional costs that you may incur without paying any income tax. This is called the Home Working Allowance.

Also, any equipment that is provided to the employee that is wholly, necessarily and exclusively for the purpose of that work is also exempt

7. Relevant life cover

This is a special sort of life insurance that the company takes out on behalf of its employees, with the employee’s family or financial dependents receiving the benefits on the death of the employee. This is a really complex and highly regulated financial service and we strongly recommend that you seek advice from a suitably qualified financial advisor before taking any action. I just wanted to make you aware that there are some sorts of life insurance products that the company can take out on your behalf. Whilst a touch grim, it may be potentially relevant in the current circumstances. Here is a useful article from Unbiased.

Conclusion

So that’s our top recommendation for tax free benefits. These are benefits that all companies should consider to help save tax. We would be more than happy to discuss this further with you if you have any questions.

When businesses are owned and run by the same person (the director is a shareholder) there are very often transactions between the company and the director. This could be the director initially putting money into the business to start it up, or injecting some cash when the company needs it. These sorts of transactions create something called a director’s loan account.

It may also be for wages that have been declared to HMRC but not yet taken, or expenses incurred by the director personally but not yet refunded to them.

The above are all transactions that increase the amount of money that the company owes the director.

However there are transactions that can send the balance in the other direction – simply drawing money out the business without declaring a dividend, or having the company the company pay for something personally for you. These are all obvious types of transaction which will either reduce the amount owing to the director, or will mean that the director actually owes the company some money.

There are other sorts of transactions that can sneak up on directors – illegal dividends are the most obvious transaction we see – where a director has paid more in dividends to themselves that company law allows them to – this would put the dividend in a repayable position.

The typical scenario is where the director has been only really paying attention to the bank account and paying themselves what is in the bank, forgetting that corporation tax is also due (this is incredibly common!)

Should the director owe the company money there are a variety of tax implications that apply.

A history of (tax) abuse

To understand the tax implications of the tax on an overdrawn director’s loan account its useful to know the context and history as to how it arose.

In the past some less that scrupulous directors would attempt to avoid paying income tax (or corporation tax) by lending themselves a large amount of money. As the money was a loan there was not income tax paid on it. This amount would continue to rack up until the directors decided to wind the company up, chalk the director’s loan as a bad debt, write it off and wind up the company.

The directors have the cash, and no impact was due. In our view this was never strictly legal but non-the-less did happen.

Section 455

To combat this HMRC brought in legislation that put the tax burden on the company – what is know as section 455. This means if there is a director’s loan balance outstanding at the year end the company has to pay tax at 32.5% on the increase in that loan. This was intended to ensure that HMRC got the tax even if the company subsequently was wound up.

There are a lot of rules around this, including the ability to get that amount back if the loan is repaid, or income tax paid on it.

Benefit in kind

On top of this s455 there is also something known as a benefit in kind that needs to be considered as well.

HMRC take the view that if you are borrowing money from the company, and not paying any interest on that money you are getting a benefit from the company and should therefore pay tax on the value of that benefit.

Thankfully this is quite a low level of benefit – the benefit is considered to be the tax you have not paid, which given the current official rate of 2.5% means that the overall tax you pay on this is often not all that much. On a £20k loan that interest should have been £500. Income tax at 40% would mean a tax charge of £200.

There is also a national insurance consideration that the company needs to pay on benefits in kind – Class 1a charged at 13.8% on the £500 totalling £69 (this £69 is tax deductible for corporation tax purposes so in reality works out to only cost £55.89). So on a loan of £20k a director might pay £255.89 per year.

The key issue with the benefit in kind that many directors find is not the cost, but remembering to do it, or paying an accountant to file the P11d form at the end of the year.

What Can I do about it?

With an overdrawn director’s loan account there are limited remedies, and non that are pain free.

Here are a range of options

Repay the loan – if it’s under £10k you may be able to repay it then draw it back out shortly after – what is known as bed and breakfasting. This, however is not recommended as there are rules in place to combat it

Declare a “paper dividend” to clear the director’s loan account. This is where you declare a dividend, but pay no cash to yourself. The real sting in the tail is that, despite having not cash from the dividend, you will still need to pay dividend tax. You can only do this if you have sufficient “distributable reserves” to do so (basically profit not yet paid as a dividend).

Declare a bonus to clear the director’s loan account. This is the same as the above option for times where there are not sufficient distributable reserves. You will pay income tax, national insurance and the company will pay employers national insurance on this so its quite expensive.

Here are some things you can’t do

Ignore it – simply – that would be illegal (tax evasion, which once you do anything with it then becomes money laundering – all very serious)

Wind the company up – HMRC would have the right to object and appoint a liquidator. They would come after you personally for the money.

Director’s loans can get quite complex so its important to account for things well and get it right. Cloud accounting software can be a real help with this (FreeAgent is particularly good for this), as can having an accountant who is alert to this issue.

Ultimately, setting up your business in an efficient and structured way can help considerably to keep you organised. Simply being aware of the issue and avoiding making any large dividends at the end of the year often helps.

One of the most tax efficient ways you can get your money out of a company is through making company pension contributions. You need to do it right to get the most from it, but it can be very effective.

Pensions are brilliant, and far from boring!

I should say that actual pension advice is a regulated area, and you will need to take specific advice on pensions from a suitably regulated financial advisor, which we are not – this is an article about saving tax through a pension).

Most people’s eyes glaze over when you talk about pensions. They have a reputation being boring, not to mention complex. Also, its something for ages away, right? Not now – I’ve got real issues that I need to deal with right now, pensions can wait.

The principle, however, is really simple – you save now, into a pension scheme (if it helps – think of it like a bank account), that money is invested in a variety of ways and is used to live on when you retire.

From a tax perspective they are very tax efficient (the government wants us to save for retirement), and so gives various tax benefits for paying into your pension fund.

What you do now makes a massive different to the future

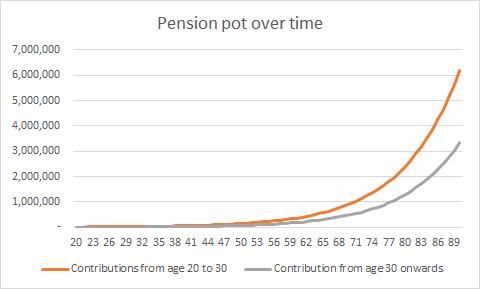

One of my favourite graphs of all time (yes, I have one!) is the one below. It shows the difference to the value of a pension pot between two scenarios. Seeing this in my 20s made a massive difference to how I acted with pensions.

The two scenarios are this

Ms Orange – an individual invests £1000 per year between the age of 20 to 30 and then stops – completely stops contributing to it.

Mr Grey – another individual only starts to invest £1000 from the age of 30 and continues forever.

Both individuals get the same return on their investments at 10%.

Not only does Ms Orange have more money at the time of retirement than Mr Grey despite having stopped investing at the age of 30.

No, the really really shocking this is that, at this investment rate Mr Grey will never, ever ever ever have more than Ms Orange. Ever!

Take a moment to let that sink in….

To me, the message was clear – start early

SIPP – your flexible tax efficient friend

To get the maximum tax saving on your pension contributions you will be in need of a self invested personal pension plan, or SIPP. These are pension plans that are owned by the individual and are a bit like ISAs, but for pensions. The point is that the company, really, has very little to do with the scheme.

Now at this point I will often hear clients talk about how they have a company pension scheme for auto-enrolment through NEST, or some other pension provider, with deductions being made through their payroll. This is one method of paying into a pension from a company, but its not the method we are talking about here, as it is really restricted to how much salary you pay, and also restricted in terms of your choice of funds to invest in. To get the big tax savings you need a SIPP.

A good place to start learning about a SIPP is through Money Saving Expert (https://www.moneysavingexpert.com/savings/cheap-sipps/) but do seek out a financial advisor to assist you if you don’t feel comfortable doing it yourself.

Tax Savings on Contributions to a SIPP

Where a company makes a contribution to a SIPP, it is treated, for corporation tax purposes, as being the same as paying salary – its a cost of employment. As such, it reduces the taxable profits in the company, and therefore you pay less corporation tax.

So long as the contributions made from the company are below £40,000 in any one tax year, the tax implications on you individually are nil. You can pay up to £40,000 from the company into a SIPP in any one personal tax year.

How to pay pension contributions into a SIPP

Each SIPP provider will be different in how they want the funds transferred, so you will have to check with them, however from a company perspective, you simply account for the contribution in the same way you would any other cost. There is no reporting to HMRC or anything complicated..

Whether you want to make a contribution on one lump sum, or make a regular contribution is to some extent a personal choice, assuming the SIPP provider allows it. You may want to look into the effects of pound cost averaging for regular investments, but this is drifting into investment advice for which you should consult a financial advisor.

As a company, there are a number of exempt benefits that are potentially available. Exempt benefits mean that the company pays for something on your behalf. The expense is deductable on its corporation bill, but you, as a director or employee do not get taxed individually.

Expenses payments and benefits you get are not always shown on your P11D. This may be because they are covered by:

a dispensation (an arrangement your employer may have with us to save you the trouble of including a benefit or expense payment that you get and then having to make a matching claim for the allowable expenses you incur)

a PAYE Settlement Agreement (where your employer settles your Income Tax liability on certain benefits in kind and expenses payments)

a statutory exemption or an Extra-Statutory Concession

You do not have to pay tax on benefits and expenses covered by concessions or exemptions. If the concessions or exemptions apply to you, do not enter the benefits and expenses concerned on your tax return.

Brief details of the most common exemptions and concessions follow.

One mobile phone provided by your employer and any line rental for and calls with that phone paid directly by your employer. Money your employer pays you to use your own mobile phone is taxable. A mobile phone provided to a member of an employee’s family or household is taxable.

Expenses of providing a pension

Expenses incurred providing any pension to be given to you or to any member of your family on your retirement or death should not be shown on form P11D. This is either because they are exempt or because they are entered elsewhere.

Payments by your employer towards additional household costs where you work at home

Payments made to you by your employer for your reasonable additional household costs if you work at home regularly, are exempt from tax and you do not need to enter them on your tax return. You need to work at home by agreement with your employer instead of working on their premises. The exemption does not apply if you simply take additional work home in the evenings. Your employer may pay you up to £4 a week without you needing to keep supporting evidence of the cost. You can pay more where your costs are greater, provided you keep supporting evidence to show that the payment is wholly for additional household expenses incurred in working at home or where your employer has agreed a figure with us.

Employee shareholders financial advice

The benefit of the employer funding certain kinds of independent advice in relation to the employee shareholder agreements is not taxable in the hands of the employee.

Accommodation, supplies and services on your employer’s business premises

Accommodation, supplies and services (for example, ordinary office accommodation, and equipment, phones, typists, messengers, stationery) provided to you on your employer’s business premises and used by you in performing your duties, provided that if there is any occasional private use of the items by you it is not significant.

Supplies and services provided to you other than on your employer’s premises

Supplies and services (for example, work equipment to use at home, stationery and consumables) provided to you to perform your duties, provided that if there is an occasional private use of the items by you it is not significant. This exemption does not apply to motor vehicles, boats or aircraft, or any extension or conversion of living accommodation or similar building work.

If you are a disabled employee and your employer provided you with special equipment to help you to work, such as a wheelchair or hearing aid, this exemption applied even if your private use of the equipment was significant because it was also used outside work.

Travel

Incidental overnight expenses

Payments that your employer makes for personal expenditure, up to certain limits, when you stay away from home for at least 1 night during a business journey. The maximum amounts that may be paid without any tax consequences are:

£5 a night for each night away during business journeys anywhere in the United Kingdom (UK) (Great Britain and Northern Ireland)

£10 a night for each night away during business journeys outside the UK

If the maximum for a business journey as a whole is exceeded, the full amount paid for that journey is taxable.

Travelling expenses of directors

Travel expenses paid to a director who gives their services without remuneration to a company not managed with a view to dividends.

Reasonable travel expenses paid to a director by the company where the directorship is held as part of a professional practice, provided no claim is made for a deduction for that expenditure by the practice.

Where a director’s spouse or partner accompanies the director on a business trip abroad because the director’s health is so precarious that the director could not undertake the foreign travel alone, the expenses borne by the employer for the spouse’s or partner’s travel on that journey. The same principle applies to employees as it does for directors.

In all cases, travel expenses include reasonable hotel expenses necessarily incurred.

Travelling expenses of group company employees

Where an employee has employments with 2 or more companies that are part of the same group of companies, any journey made between the places at which the duties of those employments are carried out is a business journey.

Travelling and subsistence expenses following strike disruption

Reasonable expenses reimbursed to you, or paid on your behalf, if, because of dislocation of public transport by strikes or other industrial action, you:

stay overnight in hotel or other accommodation

incur extra costs in travelling to and from work

Car, motorcycle and bicycle parking

The provision of car or motorcycle parking space, or facilities for parking bicycles, at or near the employee’s place of work.

Work to home travel provided when you work late or when sharing arrangements are disrupted

The cost of transport (for up to 60 journeys in the year) your employer provides to take you home if:

you are occasionally required to work later than usual (and until 9pm or later) but those occasions are irregular

by the time you can go home, either public transport between your place of work and home has ceased, or it would not be reasonable in the circumstances for your employer to expect you to use it you normally travel to and from work in a car shared with other employees

you cannot get home in the shared car because of unforeseen circumstances which could not reasonably have been anticipated

Disabled people’s cost of travel between home and work

Assistance with the cost of travelling between home and work, or to and from a place where work-related training is provided (including the reimbursement of travel expenses), given to people with a substantial and long-term disability.

In addition, a car provided for these purposes is not taxed if:

you are disabled

the car has been adapted to the needs of your disability (or, if you are unable to drive a car with manual transmission, is equipped with automatic transmission)

other private use by you or anyone else is prohibited

there is no other private use of the car

Work buses and subsidies to public buses

The benefit of travel between home and work in a work’s bus or minibus provided that:

the bus or minibus has a seating capacity of 9 or more

the bus is available to all employees

substantially the whole use of the service is by employees (and their children)

Or if your employer pays a subsidy to a public bus service and in return you receive the benefit of an enhanced service on that route and/or you travel at reduced cost or no cost on that route, provided that the service on that route is available to all employees.

Bicycles and cycling safety equipment

The benefit of a bicycle and/or cyclist’s safety equipment (or a voucher to obtain these) lent to you, provided that:

such bicycles and equipment are available generally to employees of your employer

your main use of the bicycle is for journeys between home and work or between workplaces

The benefit of a meal or refreshments provided to you after you cycled to work on a day designated by your employer as a ‘cycle to work’ day.

Healthcare, wellbeing and childcare

Health screening and medical check-ups

Expenses incurred in providing you with a maximum of 1 health screening assessment and 1 medical check-up in any year.

‘Health screening assessment’ means an assessment to identify employees who might be at particular risk of ill-health.

‘Medical check-up’ means a physical examination of the employee by a health professional for (and only for) determining the employee’s state of health. This exemption does not cover medical treatment.

Medical treatment abroad

The cost of necessary medical treatment abroad paid for by your employer, or paid by you and reimbursed to you by your employer, where you fall ill or suffer injury while away from the United Kingdom in the performance of your duties. The cost of providing insurance for you against the cost of such treatment is also non-taxable.

Counselling

Most counselling services provided in connection with termination of employment are exempt from tax. There are detailed conditions. Ask us or your tax adviser for more information.

Welfare counselling

Welfare counselling made available to all employees generally on similar terms is exempt from tax. For this purpose, welfare counselling does not include:

any medical treatment

advice on finance or tax (other than debt counselling)

advice on leisure or recreation

legal advice

Nurseries and playschemes

Places in nurseries or playschemes on premises made available by your employer or, if your employer runs the nursery jointly with others, on premises made available by 1 or more of those others, provided that your employer participates in managing and financing the provision of care.

Childcare vouchers

Qualifying childcare vouchers up to the appropriate amount for a week are not taxed. If you receive more than the appropriate amount for a week in childcare vouchers, the excess over the appropriate amount is taxable and you should include it on your tax return. If your employer has given you childcare vouchers with a value greater than the appropriate amount, your employer will enter only the taxable amount on your P11D. You can find more information on qualifying childcare vouchers, including how the appropriate amount is calculated, at EIM16050 in the Employment Income Manual.

Other employer-supported childcare

Where your employer contracts directly with a commercial nursery to provide qualifying childcare for a child for whom you have parental responsibility, the appropriate amount for a week is not taxed. If the cost incurred by your employer is greater than the appropriate amount for a week, the excess over the appropriate amount is taxable and you should include it on your tax return. If your employer provided directly contracted childcare for your benefit at a cost greater than the appropriate amount, your employer will enter only the taxable amount on your P11D. You can find more information on directly contracted childcare, including how the appropriate amount is calculated, at EIM22010 in the Employment Income Manual.

Training

Employer-funded or employer-reimbursed training

This exemption covers the costs borne by your employer of work-related training within the whole range of practical or theoretical skills and competences you are reasonably likely to need in your present or likely future jobs with your employer. The exemption extends to:

training activities such as first aid and health and safety in the workplace

employee development schemes

activities intended to develop skills you need in leadership and teamwork, for example, Raleigh International

training which is provided by a third party rather than your employer

All the ways in which training can be delivered are covered, including full-time and part-time training, internal training courses run by your employer, courses which are run externally or by a third party, and courses which comprise any mixture of these.

The tax exemption also covers:

travel and subsistence expenses, to the same extent as if you were undertaking employment duties while training

other incidental costs, such as additional childcare expenses directly related to you undertaking the training in question

costs which relate to examinations and registration of qualifications

the costs of multi-media and distance-learning aids, practical course materials and books

Training, or training-related travel and subsistence, which is provided as entertainment, recreation, reward or an inducement, remains taxable. Any asset provided to you or for your use is also taxable unless the asset is provided or used purely for training, or for training coupled only with use in the performance of the duties of your office or employment. Assets provided for private use remain chargeable in the normal way.

Certain retraining costs

Costs met by your employer for you if you are about to leave your employment, or have left within the previous year, to allow you to attend certain courses of retraining intended to help you get another job.

If you have not left by the time you start the course, you must leave within 2 years of finishing it for the exemption to apply. The exemption is withdrawn if you are re-employed by the same employer in the 2 years following the end of the course. (The employer must tell us within 60 days of this happening.)

Exemption is only available if you have been employed by your employer for at least 2 years up to the time you begin the course (or at the time the employment ceased).

Courses must:

teach or improve skills which will help you to find new work (and be entirely devoted to those objectives)

last no more than 2 years

The opportunity to attend courses must have been given to all employees in a similar position.

Exempt expenses are:

fees for the course

fees for examinations taken during or at the end of the course

the cost of essential books

the full cost of travelling to attend the course, plus related subsistence expenses

Gifts, entertainment and awards

Long service awards

Long service awards made to directors and employees as testimonials to mark long service where the service is not less than 20 years and no similar award has been made within the previous 10 years. These have to be one of the following:

tangible articles of reasonable cost

shares in an employing company (or another company in the same group)

The cost of an article is taken as reasonable where it does not exceed £50 for each year of service.

Suggestion schemes

Awards made to you under a suggestion scheme where your employer’s scheme is open on the same terms to all their employees a particular category of them. For example, a scheme which is open to all employees in a particular geographical area will satisfy this condition.

The scheme must meet the following conditions that the suggestion:

must relate to the activities carried on by your employer

is made is outside the scope of your normal duties – the test is that, taking account of your experience, you could not reasonably have been expected to put forward such a suggestion as part of the duties of your post

was not made at a meeting held for the purpose of proposing suggestions

The exemption applies to 2 types of awards for suggestions encouragement awards and financial benefit awards.

Encouragement awards

An encouragement award made for a suggestion which reflects praiseworthy effort on the part of the person making the suggestion. The permitted maximum for an encouragement award is £25. If the encouragement award exceeds £25 the excess over £25 is taxable.

Financial benefit awards

There are additional conditions which apply to financial awards.

Awards should only made following a decision to implement the suggestion.

The decision to make an award is based on the degree of improvement in efficiency likely to be achieved. This is measured by the prospective financial benefits and the period over which they would accrue the importance of the subject matter having regard to the nature of the employer’s business.

The amount of the award does not exceed 50% of the expected net financial benefit during the first year of implementation 10% of the expected net financial benefit over a period of up to 5 years subject, in each case, to an overriding maximum of £5,000 – where an award exceeds £5,000, the excess over that figure is taxable.

If 2 or more employees receive an award in respect of the same suggestion, the exempt amount is divided between them in the same proportion as their individual awards bear to the total sum awarded.

Goodwill entertainment

Providing goodwill entertainment for an employee, or for a member of the employee’s family or household, provided that:

the person providing the entertainment is neither the employer, nor a person connected with the employer

neither the employer nor a person connected with the employer has directly or indirectly procured the provision of the entertainment

the entertainment is neither in recognition of particular services which the employee has performed or in anticipation of particular services which are to be performed by the employee in the course of their employment

This exemption applies only when the cost of the entertainment is taxable under Section 87 (vouchers), Section 94 (credit tokens) or Section 201 (benefits in kind). It does not extend to liability under Section 62 (earnings) or Section 72 (taxable expenses payments). The section numbers mentioned here refer to the Income Tax (Employments and Pensions) Act 2003.

Certain gifts

Certain gifts from third parties if all these conditions are satisfied the gift:

consists of goods or a voucher or token only capable of being used to obtain goods

person making the gift is not your employer or a person connected with your employer

is not made either in recognition of the performance of particular services in the course of your employment or in anticipation of particular services which are to be performed

has not been directly or indirectly procured by your employer or by a person connected with your employer

cost the donor £250 or less and the total cost of all gifts made by the same donor to you, or to members of your family or household, during the tax year is £250 or less

Some other gifts are not taxable. If you earn at a rate of less than £8,500 a year and you are not a director, a gift to mark a personal occasion, such as a wedding present, which is not a reward of your employment, is not taxable. If you earn at a rate of £8,500 or more a year, or you are a director, any gift from your employer is taxable unless your employer is an individual and makes the gift in the course of family, domestic or personal relationships.

Christmas or other annual party

Annual parties or alternative functions, such as a Christmas dinner and a summer party. These events should be open to staff generally and cost no more than £150 a head in total to provide.

Sports facilities

Sports facilities generally available to all employees and members of their families and households. This does not apply to facilities:

available to the general public

consisting of, or provided in association with, overnight or holiday accommodation

provided on domestic premises

consisting of mechanically propelled vehicles or vessels such as cars, motorboats and aeroplanes

Loans for a purpose that attracts tax relief in full